The best legal strategies for protecting families from long-term care costs are almost never “one document” or a quick transfer. In our Brooklyn practice, we meet middle-income caregivers and small business owners who did everything right, paid off the co-op, saved consistently, then got blindsided by a nursing home bill that can rival a mortgage in Manhattan.

The good news is that a coordinated plan can protect a home, stabilize family finances, and reduce stress when care decisions get urgent. This guide walks you through Medicaid planning, irrevocable trusts, and LLC-based protections, in plain English, with Brooklyn-specific examples. If you are starting from zero, begin by learning what Medicaid does (and doesn’t) cover in New York.

Ready to get a clear plan, not just general information? Schedule a Free Consultation with Alatsas Law Firm to discuss your family’s goals and timeline.

Key Takeaways

- Long-term care costs compound fast: A few months of private pay can force rushed decisions that permanently reduce what a family keeps.

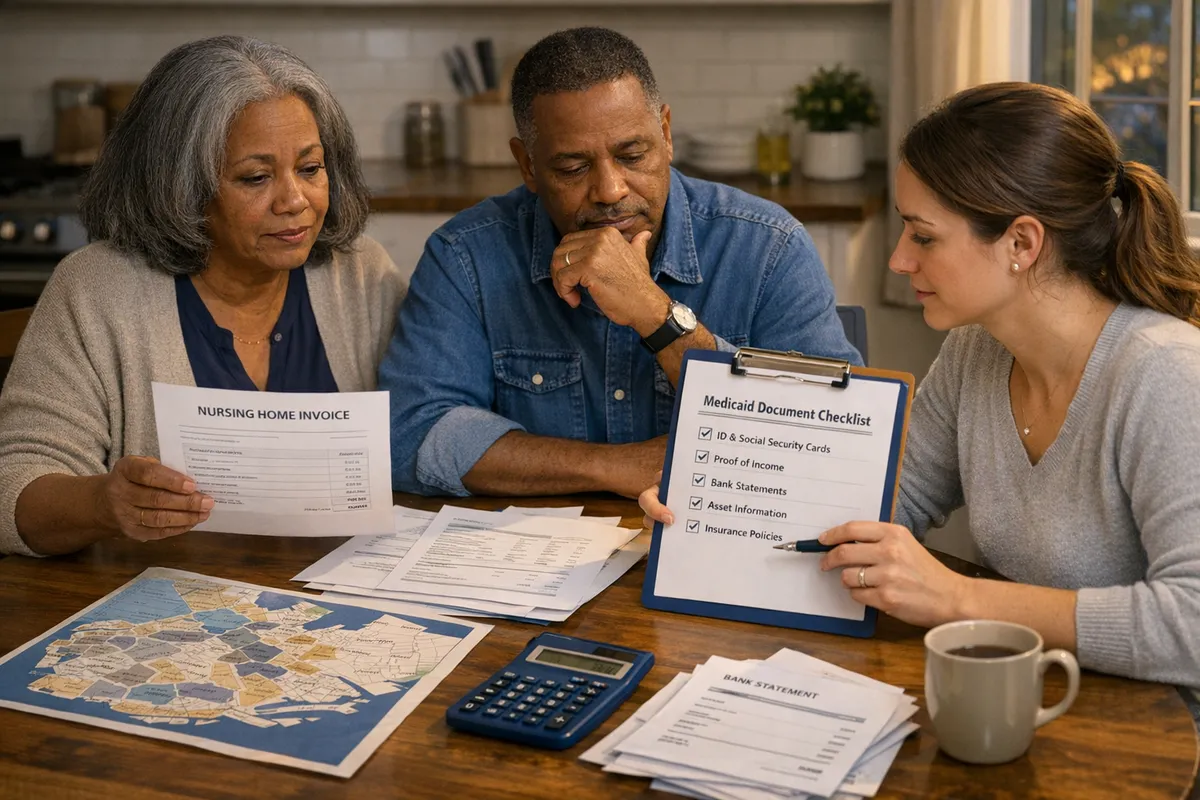

- Medicaid eligibility is paperwork-heavy: Best legal strategies for protecting families from long-term care costs include organizing records early and using the right exemptions.

- Irrevocable trusts can protect the home: Timing and “control” rules matter more than the form itself.

- LLCs can separate business risk: They may also help structure rental or investment property ownership, but they are not a magic Medicaid shield.

- Coordination beats one-off fixes: Medicaid planning, trusts, and LLCs work best when designed as one system.

Understanding the High Costs of Long-Term Care and Its Impact on Brooklyn Families

Sticker shock is the first reason families lose assets, not bad intent. In Brooklyn, a private-pay nursing home stay can burn through retirement savings quickly, and home care hours add up just as fast when a parent needs round-the-clock help.

A common scenario is a daughter in Bay Ridge juggling work and caregiving while trying to “hold the line” on spending. The family pays privately for aides for a few months, then a hospitalization turns into rehab, then rehab turns into a longer stay. By the time Medicaid comes up, the family is already in crisis mode, with bills, facility deadlines, and incomplete paperwork.

For small business owners, the pressure is different. Cash flow is tied to payroll, inventory, and leases. If mom needs care, the family may pull money from the business, skip estimated taxes, or liquidate a retirement account at the worst time. In our experience, that kind of emergency spending is what makes later Medicaid planning harder.

A Brooklyn case study (anonymized)

A Marine Park family came in after spending down substantial savings on home care. The adult children feared the family home would be next. Once we mapped out their assets and care needs, we identified which resources were countable, what could be restructured, and what documentation would be needed to move forward. We also discussed responsibility myths, because families often worry their own savings will be taken. If that fear sounds familiar, read Avoid Burdening Your Children With the Cost of a Nursing Home Stay.

The next step is turning anxiety into a timeline, because best legal strategies for protecting families from long-term care costs depend heavily on when care is needed.

Step-by-Step Elder Law Planning in Brooklyn: Navigating Medicaid and Eligibility

Medicaid planning works best when you treat it like a project with phases, not a single application. Brooklyn Medicaid planning for families often succeeds or fails based on organization, timing, and avoiding well-meaning “quick fixes” like informal gifting.

Below is a practical step-by-step elder law planning in Brooklyn blueprint we use to reduce surprises.

Step 1: Clarify the care path and benefits you are really seeking

Start by identifying whether the immediate need is home care, assisted living, or skilled nursing. Coverage differs, and confusion is common. Our clients often benefit from reading What Medicaid Does (and Doesn’t) Cover in New York before they take action. For official baseline information, you can also review New York’s Medicaid resources at the New York State Department of Health.

Step 2: Inventory assets and income the way Medicaid will view them

Make a clean list of bank accounts, retirement accounts, life insurance cash value, real estate, and any transfers in recent years. Eligibility is not just about what you own today, but what you did recently. We routinely see families underestimate how much documentation Medicaid requires, especially for multiple accounts.

Step 3: Avoid panic gifting and “add my child to the deed” mistakes

Gifting money prior to nursing home admission can create penalties depending on timing and facts. Similarly, changing title to a home without understanding the consequences can trigger Medicaid issues and tax problems. If you are considering a trust, start with this plain-language overview: When should a family consider a trust as part of an estate plan, and what type of trust should they use?.

Step 4: Use short-term bridges when a crisis hits

Not every family has years to plan. When timing is tight, we look at lawful crisis strategies, including whether benefits can help retroactively. In some cases, retroactive coverage can prevent financial disaster after a hospitalization or sudden placement. See Using Retroactive Medicaid Benefits to Prevent Financial Disaster.

Step 5: Submit a complete application and plan for follow-up

A strong application package reduces delays. Expect requests for additional proof. When families budget time for follow-up, they avoid missed deadlines and unnecessary denials.

This is where best legal strategies for protecting families from long-term care costs meet real life: you need a plan you can execute while also caring for your parent.

How to Use Irrevocable Trusts for Asset Protection Against Long-Term Care Costs

An irrevocable trust can be a powerful tool, but only if it is drafted, funded, and timed correctly. When people search how to use irrevocable trusts for asset protection, they are usually trying to answer one question: “Can a nursing home take my house if it is in a trust?” The truthful answer is, it depends on the trust type, when it was created, and whether the assets were properly transferred.

In New York, a properly structured Medicaid Asset Protection Trust is often used to protect a home and certain savings from being depleted by long-term care expenses. The trust has a trustee, rules for distributions, and restrictions that keep the assets from being treated as available resources for Medicaid purposes after the applicable lookback period.

What “control” really means in a Brooklyn trust plan

Families get tripped up by control. If the parent can demand principal back, or if the trust is not truly irrevocable in practice, the protection can fail. We explain this in plain English during planning meetings: asset protection comes from giving up certain rights, not from signing a form.

A Sheepshead Bay example: a widowed homeowner wanted to protect a row house while keeping the ability to live there. We structured the plan so she retained the right to reside in the home, while shifting ownership into the trust. That preserved stability for her and reduced the risk that care costs would force a sale.

If you are considering this step, review Should I put my primary residence in an irrevocable trust?.

Even with a strong trust, best legal strategies for protecting families from long-term care costs also account for non-financial assets. We often remind families to plan for personal property and keepsakes as well, because conflict over “stuff” can be just as damaging as conflict over money. A helpful starting point is Memory Makers: Your Personal Possessions.

Utilizing LLCs for Protecting Family Assets from Nursing Home Costs: What Brooklyn Business Owners Should Know

An LLC is mainly a liability and ownership tool, not a Medicaid eligibility shortcut. When people ask, “Does an LLC protect assets from nursing home costs?” they are often mixing two separate risks: business lawsuits and long-term care spend-down.

For a Brooklyn business owner, LLCs for protecting family assets from nursing home costs can still be part of the solution in specific situations. For example, an LLC may help separate a family-owned rental property from the operating business, clarify who owns what, and reduce exposure if the business is sued. That separation can preserve value for the spouse or children, even if the parent later needs Medicaid planning.

An anonymized example from Bensonhurst: a contractor had a personal account paying business expenses, plus a jointly owned rental. We helped reorganize the ownership and documentation so the lines were clearer. Clear structure reduces “messy” paperwork later, which matters when Medicaid asks for proof.

LLCs can help, but they work best when paired with elder law planning and the right trust strategy.

Coordinating Legal Strategies: Integrating Medicaid Planning, Trusts, and LLCs for Brooklyn Families’ Asset Protection

The strongest plans connect the dots between eligibility rules, family goals, and what you actually own. In practice, the best legal strategies for protecting families from long-term care costs often look like a three-part system.

First, Medicaid planning sets the timing and documentation strategy so you are not improvising under pressure. Second, an irrevocable trust can protect the home or savings when the timeline allows. Third, an LLC can cleanly separate business or rental risks, which is especially valuable for entrepreneurs who cannot afford a lawsuit plus a care crisis.

A quick gut-check we use with families in neighborhoods like Midwood and Dyker Heights is simple: if one parent needs care, does the other spouse still have enough to live on, and do the adult children understand their role? If not, start by having the conversation. This guide can help: Discussing Your Parent’s Financial Future.

Frequently Asked Questions About Protecting Assets From Long-Term Care Costs in New York

How do I avoid losing my home to pay for long-term care?

You may be able to protect your home by planning before a crisis and using the right legal structure, such as a properly drafted irrevocable trust or other Medicaid-compliant strategies, depending on your facts. The key is timing and correct ownership, because last-minute transfers can create penalties. If your family is already facing a sudden placement, crisis planning and retroactive benefits may still help.

Can a nursing home take money from an irrevocable trust?

Typically, properly protected trust principal is not “reachable” just because a nursing home bill exists, but details matter. If the trust allows the parent to access principal freely, or if the trust was not funded correctly, the assets may still be treated as available for Medicaid and effectively at risk. Trust drafting, trustee selection, and funding steps must match Medicaid rules.

Does an LLC protect assets from nursing home costs?

An LLC can help separate liability and clarify ownership, but it does not automatically shield assets from Medicaid spend-down rules. Medicaid focuses on what the applicant owns and can access. If the applicant owns an LLC interest, it can still be evaluated. LLCs are most useful when coordinated with Medicaid planning and trust planning to address both lawsuit risk and care-cost risk.

Your Next Steps: Building a Brooklyn Plan You Can Actually Execute

A realistic plan beats a perfect plan that never gets implemented. The best legal strategies for protecting families from long-term care costs start with an honest inventory, a clear caregiving timeline, and documents that match how Brooklyn families actually live and work.

If your parent is healthy, you have more options and more leverage. If a crisis is already here, you still have choices, but you need to move carefully and document everything.

Want a step-by-step roadmap tailored to your home, savings, and business? Start Your Journey with Alatsas Law Firm and get a coordinated plan for Medicaid, trusts, and asset protection.