Every Brooklyn family wants to protect their parents’ well-being and their own financial future when health issues appear. Facing rising long-term care costs, families often feel overwhelmed by confusing Community Medicaid rules and persistent myths about eligibility. By demystifying Community Medicaid eligibility and estate planning, you can safeguard your loved ones and avoid costly mistakes that strip savings or lead to denied coverage. Discover the real facts and proven strategies that help New York families confidently plan ahead.

Key Takeaways

Defining Community Medicaid and Common Myths

Community Medicaid is a state-administered health coverage program designed specifically for low-income individuals and families who don’t qualify for institutional Medicaid. Unlike facility-based Medicaid, which covers nursing home care, Community Medicaid helps eligible residents access healthcare services while remaining in their own homes and communities. It’s a crucial distinction because it shapes both eligibility requirements and asset protection strategies for Brooklyn families.

Here’s how Community Medicaid and Institutional Medicaid differ in key areas:

The program operates under federal guidelines, but each state administers Medicaid differently, which means New York’s Community Medicaid rules differ significantly from neighboring states. This variation explains why your neighbor’s application was approved while you were denied, even though your financial situations look identical. Income limits, asset thresholds, and covered services vary by state and sometimes even by county.

Myth #1: “All Medicaid is the same everywhere.” Not true. One person might qualify in New York but wouldn’t in New Jersey. The program name might sound identical, but the actual rules are anything but. This is why working with someone familiar with New York’s specific requirements matters enormously.

Myth #2: “If you own a home, you automatically don’t qualify.” This one trips up many families. Community Medicaid has specific home equity rules that differ from institutional Medicaid. Your primary residence receives special treatment and doesn’t count against eligibility in the same way other assets do, though there are important limits and exceptions.

Myth #3: “You can apply anytime and get instant coverage.” While coverage can begin immediately upon eligibility, the application process itself takes time. Incomplete applications get rejected, and reapplication costs you weeks. Starting early prevents scrambling when your parent’s health takes a sudden turn.

Myth #4: “Community Medicaid and Medicare are the same program.” They’re completely separate. Medicare is federal and based on age or disability history. Community Medicaid is state-run and based on income and assets. Many elderly Brooklynites qualify for both, but they serve entirely different purposes.

Pro tip: Get a clear understanding of your state’s specific rules before your parent needs long-term care. Apply well before a health crisis forces urgent decisions, since rush applications often contain errors that trigger denials.

Key Eligibility Rules and Income Limits for 2026

Community Medicaid eligibility in New York hinges on two primary factors: your income and your assets. Both must fall below specific thresholds set by the state. For 2026, the Federal Poverty Level standards have increased 2.6%, meaning a family of four in most states faces a poverty guideline of $33,000. New York typically uses percentages of this baseline to determine who qualifies, so understanding these numbers directly impacts your family’s eligibility.

Income calculations use a specific method called Modified Adjusted Gross Income (MAGI). This approach considers your gross income minus certain deductions, rather than looking at net income after taxes and expenses. MAGI simplifies eligibility determination across Medicaid, marketplace plans, and other programs, making applications more straightforward. However, the key word is “more”—not simple. Different household members count differently, and earned versus unearned income receives different treatment.

New York covers mandatory groups including low-income families, pregnant women, children, and seniors. Most adults qualify if their household income falls below 133 percent of the Federal Poverty Level, though some categories have higher limits. For instance, pregnant women may qualify at higher income levels than general adult populations. Asset limits are equally important but often misunderstood.

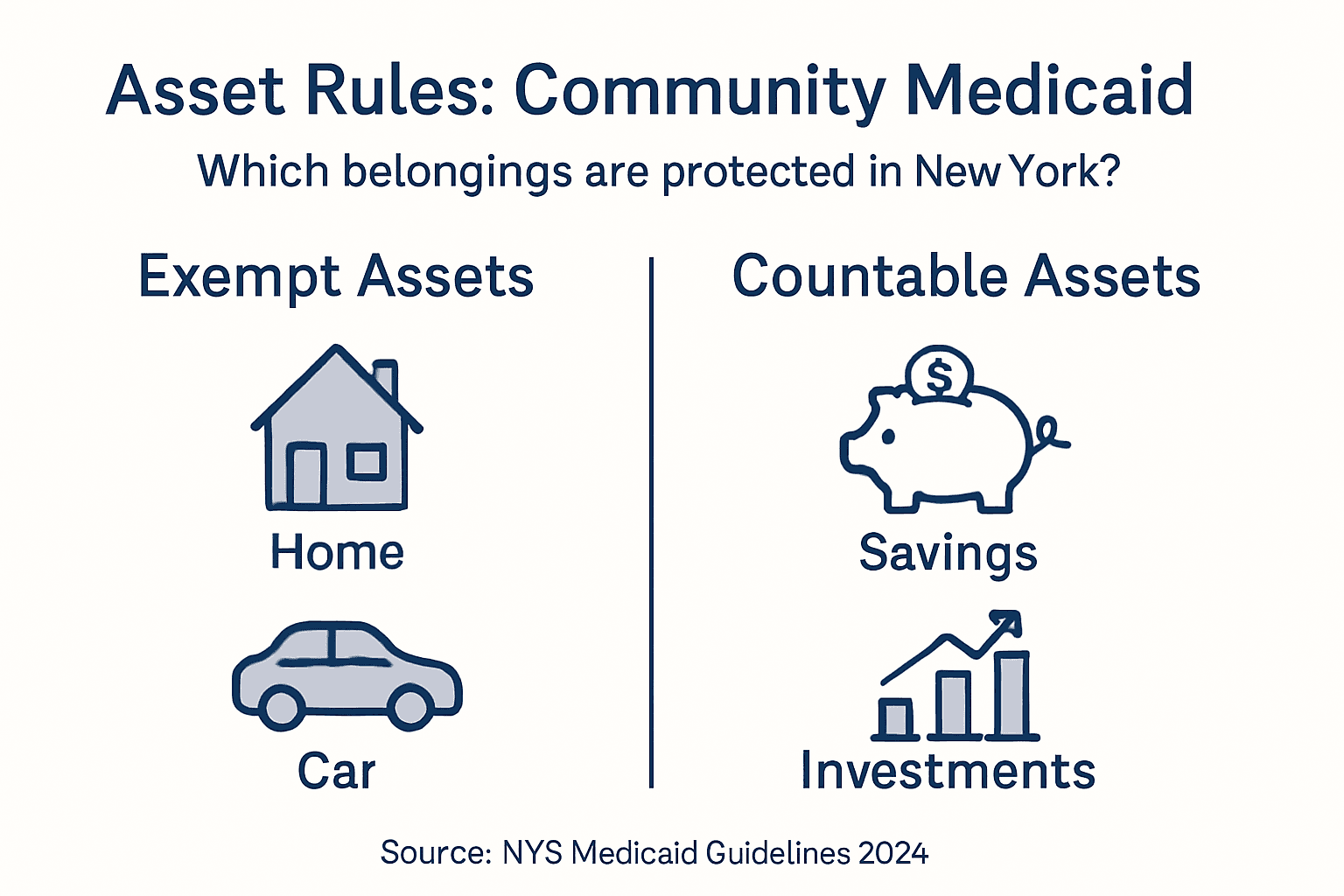

Your countable assets must stay below $15,900 for a single person or $23,850 for a couple (these limits update annually). Your primary home doesn’t count toward this limit, which matters enormously for Brooklyn homeowners. However, vacation properties, investment real estate, and rental income do count. Vehicles used for transportation are exempt up to certain values, but additional vehicles don’t receive the same protection.

Bankruptcy, inheritance, and recent gifts can complicate matters. The state looks back five years to spot transfers made specifically to qualify for Medicaid. This is why timing and strategy matter when planning ahead for your family’s long-term care needs.

Pro tip: Calculate your exact income using the MAGI method, not your take-home pay, to get an accurate picture of your Medicaid eligibility before you apply.

Types of Community Medicaid Services Available 💚

Community Medicaid covers far more than basic doctor visits. The program includes inpatient and outpatient hospital services, prescription drugs, laboratory tests, and preventive care. Your parent can access emergency room treatment, specialist consultations, and diagnostic imaging without worrying about catastrophic bills. This breadth of coverage explains why Community Medicaid matters so much for Brooklyn families facing healthcare costs that would otherwise drain savings.

Mental health and substance abuse services receive special attention under Community Medicaid. If your aging parent struggles with depression, anxiety, or past addiction issues, the program covers therapy sessions, psychiatric evaluations, and medication management. These services address real challenges that many seniors face but often hesitate to seek because of cost. New York has expanded coverage options beyond what some states offer, which is a genuine advantage.

Home and community-based services form the heart of Community Medicaid for seniors wanting to age in place. This includes home health aides who assist with bathing, dressing, and medication management. Personal care attendants can help with activities of daily living while your parent remains in their own home. Some programs even allow family members to become paid caregivers, keeping money within the family while ensuring quality care.

Long-term care services include adult day programs where seniors receive supervision, meals, and social activities while remaining independent. These programs reduce isolation and provide respite for family caregivers managing round-the-clock responsibilities. Transportation to medical appointments and community services also falls under coverage in many cases.

Optional services vary by state and can include dental care, vision services, and hearing aids. New York offers more generous optional coverage than neighboring states. Durable medical equipment like walkers, wheelchairs, and hospital beds are covered when medically necessary. Understanding your state’s specific offerings prevents surprises when you need services.

Pro tip: Request a complete list of covered services from your local Medicaid office and ask specifically about services your parent already needs rather than assuming they’re excluded.

How Asset Protection Works with Community Medicaid

Community Medicaid wasn’t designed to strip families of everything they own. The program includes built-in protections that allow you to preserve assets while still qualifying for coverage. Understanding these protections separates families who lose their life savings from those who protect their inheritance.

Not all assets count equally. Your primary residence, personal vehicle, and household furnishings are exempt from asset limits regardless of their value. This distinction matters enormously for Brooklyn homeowners. Your $800,000 house doesn’t disqualify you from Community Medicaid the way $800,000 in a savings account would. The program recognizes that some assets represent your family’s foundation, not disposable wealth.

This summary shows major asset categories and how they affect Medicaid eligibility:

Spousal impoverishment rules protect your spouse if one partner requires long-term care. Without these protections, the healthy spouse would face poverty while the other spouse qualified for Medicaid. New York law allows the community spouse to retain approximately half of joint assets up to a maximum threshold, plus a monthly income allowance. This means your marriage doesn’t become a financial catastrophe when one partner needs extended care.

Lawful asset protection strategies can include irrevocable trusts, gifts to family members, and strategic spend-downs. The timing matters critically. Medicaid looks back five years to identify transfers made with the intent of qualifying for benefits. But transfers made for other reasons, executed properly, can protect assets legally. This is where planning ahead becomes invaluable rather than scrambling when a health crisis forces immediate action.

Spend-down strategies involve using countable assets for legitimate purposes before they trigger Medicaid disqualification. Home modifications, vehicle purchases, or funeral planning can reduce countable assets while improving your parent’s quality of life. These aren’t tricks. They’re lawful strategies built into the program’s structure.

Pro tip: Begin asset protection planning at least five years before you anticipate needing Medicaid benefits to maximize your legal options and protect your family’s wealth.

Risks, Planning Mistakes, and Legal Strategies

Many Brooklyn families stumble into Medicaid planning without understanding the real risks. The biggest mistake is waiting until a health crisis forces rushed decisions. When you scramble to qualify for benefits after a stroke or cancer diagnosis, you lose access to the five-year lookback period that could have protected your assets. Time is your most valuable planning tool, and once it’s gone, no strategy can recover it.

Incomplete or inaccurate applications trigger denials that cost months of reapplication. Missing documents, miscalculated income, or undisclosed assets can disqualify you even if you technically qualify. Many families don’t realize their application failed until they’re already counting on Medicaid coverage. Double-checking every detail before submission prevents this costly delay.

Unplanned asset transfers create serious problems. Gifting money to children or paying off debts without understanding the five-year lookback can create a penalty period where Medicaid coverage gets delayed. You might think you’re helping your family, but you’re actually disqualifying yourself. The state penalizes improper transfers by making you ineligible until you’ve spent down enough assets to cover the transfer amount.

Administrative changes and reporting requirements can suddenly shift Medicaid eligibility. Missing a recertification deadline or failing to report income changes can result in unexpected coverage loss. Your parent might not realize their benefits ended until they receive a medical bill they assumed was covered. Regular check-ins with your Medicaid caseworker prevent these surprises.

Legal strategies protect you when executed properly and early. Irrevocable trusts, spousal asset protection, and strategic spend-downs work because they follow state and federal rules explicitly. But timing matters absolutely. These strategies lose effectiveness or become impossible if you wait until your parent needs care tomorrow.

Common mistakes also include failing to understand how different assets affect eligibility differently. Retirement accounts have different rules than bank accounts. Life insurance has different rules than investment property. Treating all assets the same leads to unnecessary asset loss that proper planning could have prevented.

Pro tip: Schedule a consultation with a Medicaid planning attorney at least three years before you anticipate needing benefits, not when the health crisis happens.

Protect Your Family’s Future with Expert Community Medicaid Planning

Facing the complex challenges of Community Medicaid can feel overwhelming for Brooklyn families. Understanding eligibility rules, the five-year lookback period, and asset protection strategies is essential to safeguard your loved ones from unnecessary financial hardship. This article highlights critical points that many families miss such as the differences in Medicaid rules, protecting your home, and avoiding costly application mistakes.

At Alatsas Law Firm, we specialize in elder law and Medicaid planning, guiding families through every step to protect assets and secure long-term care options. Don’t wait until a health crisis hits to take action. Our personalized approach helps you navigate New York’s specific Medicaid rules with confidence and peace of mind. Learn more about how we can help you by visiting our contact page.

Start your planning today to avoid delays and preserve your inheritance. Schedule a consultation with our experienced team and discover tailored legal strategies designed to meet your family’s unique needs. Visit Alatsas Law Firm Contact to take the first step towards securing your family’s future.

For additional resources on estate and elder law, explore our informative guides and FAQs on our website. Protecting your assets and ensuring quality care is possible with the right legal help on your side.

Frequently Asked Questions

What is Community Medicaid?

Community Medicaid is a state-administered health coverage program for low-income individuals and families who do not qualify for institutional Medicaid. It provides access to healthcare services for eligible residents while they remain in their own homes and communities.

How do income and asset limits affect Community Medicaid eligibility?

To qualify for Community Medicaid, both your income and assets must fall below specific thresholds set by the state. Income is calculated using Modified Adjusted Gross Income (MAGI), while countable assets must remain below $15,900 for an individual or $23,850 for a couple, with certain exemptions for primary residences and vehicles.

What kind of services are covered under Community Medicaid?

Community Medicaid covers a wide range of services, including inpatient and outpatient hospital services, prescription drugs, mental health services, home health aides, personal care attendants, and optional services like dental and vision care, among others.

How can families protect their assets while applying for Community Medicaid?

Families can protect their assets through various strategies, such as using irrevocable trusts, making appropriate gifts, and planning spend-downs. It’s essential to begin planning ahead of time, ideally five years before applying, to maximize legal protections while adhering to the five-year lookback rule.

Recommended

- Brooklyn Medicaid Asset Protection Trust Lawyer | Alatsas Law Firm | Alatsas Law Firm

- How to Prevent Being Disqualified for Medicaid Eligibility | Alatsas Law Firm

- Protect Your Family’s Inheritance from Medicaid Spend-Down | Alatsas Law Firm

- Medicaid Planning Guide for Middle Income Families in NY | Alatsas Law Firm