Every family in Brooklyn with aging parents hoping to protect a lifetime of savings faces big questions when urgent long-term care needs surface. As Medicaid eligibility rules become more complicated and administrative hurdles threaten coverage, the fear of losing hard-earned assets to nursing home costs grows. This guide breaks down what crisis Medicaid planning truly means for middle-income families and highlights crucial strategies for protecting your family’s future when time is running out.

Key Takeaways

| Point | Details |

|---|---|

| Urgent Need for Crisis Planning | Crisis Medicaid Planning is essential for families facing immediate long-term care needs, requiring swift asset protection strategies. |

| Complexity of Medicaid Regulations | Families must navigate stringent eligibility requirements and asset limits to maintain Medicaid coverage and prevent penalties. |

| Professional Guidance is Crucial | Consulting an elder law attorney is vital to effectively implement strategies that protect family assets during crises. |

| Comparative Benefits of Advance Planning | Advance Medicaid planning allows for more flexible asset protection options, significantly reducing the risk of penalties compared to crisis planning. |

Crisis Medicaid Planning Defined and Debunked

Crisis Medicaid Planning represents an urgent legal strategy designed to protect a family’s financial assets when a senior requires immediate long-term care. Unlike traditional planning approaches, crisis planning occurs when an elder needs nursing home care immediately, with little to no prior preparation. The goal is simple: preserve as many assets as possible while qualifying for Medicaid benefits.

Understanding this process requires recognizing the severe challenges faced by families. Medicaid eligibility challenges create significant administrative hurdles where millions can lose critical healthcare coverage rapidly. These complexities make proactive asset protection strategies not just beneficial, but essential for middle-income families facing potential long-term care needs.

The core strategies of crisis Medicaid planning typically involve asset restructuring, strategic spend-down techniques, and legal mechanisms like specific trusts or transfers that help individuals qualify for Medicaid without completely depleting their life savings. Families must navigate complex rules around income limits, asset thresholds, and transfer penalties - which is why professional legal guidance becomes crucial in these time-sensitive scenarios.

Pro tip: Consult an elder law attorney immediately when a nursing home placement becomes imminent to maximize your asset protection strategies and avoid costly Medicaid penalties.

When Crisis Medicaid Planning Becomes Necessary

Crisis Medicaid planning becomes imperative when families face sudden, unexpected long-term care needs with limited time for strategic financial preparation. Typically, this scenario unfolds when a senior requires immediate nursing home placement or intensive medical care, leaving little room for traditional asset protection strategies. The urgency stems from the complex eligibility requirements and strict financial limitations imposed by Medicaid programs.

Medicaid coverage challenges create significant barriers for families seeking immediate assistance. As states resume eligibility reviews and disenrollment processes, many individuals find themselves navigating a complex system with rapidly changing rules. These administrative hurdles mean families must act quickly to protect assets and maintain crucial healthcare coverage.

Key triggers for crisis Medicaid planning include sudden health deterioration, unexpected medical diagnoses, or abrupt need for long-term care services. Families must be prepared to make rapid financial decisions, including asset restructuring, strategic spend-downs, and potential transfers that comply with Medicaid’s intricate regulations. Professional legal guidance becomes critical in these time-sensitive situations to prevent potential penalties and ensure maximum asset preservation.

Pro tip: Document all financial transactions and medical needs meticulously when preparing for a potential Medicaid application to streamline the eligibility determination process and minimize potential complications.

Types of Urgent Asset Protection Strategies

Crisis Medicaid planning demands sophisticated asset protection strategies that can be implemented rapidly to preserve family wealth while maintaining Medicaid eligibility. The most critical approaches include spousal asset transfers, irrevocable trust formations, and strategic spend-down techniques designed to shield resources from potential spend-down requirements while navigating complex Medicaid regulations.

One innovative approach involves community-based crisis interventions, which can help families strategically manage healthcare needs while protecting financial resources. These strategies often involve creating legal mechanisms that redirect assets without triggering Medicaid penalties, such as converting countable assets into exempt resources or utilizing specific transfer strategies that maintain family financial stability.

The most effective urgent asset protection strategies typically include:

- Establishing Medicaid Asset Protection Trusts

- Implementing spousal refusal provisions

- Converting excess resources into permissible exempt assets

- Utilizing specific gift and transfer strategies that comply with Medicaid lookback rules

Professional legal guidance becomes paramount in executing these complex strategies, as each approach requires precise timing, documentation, and compliance with state-specific Medicaid regulations. Families must act swiftly and strategically to maximize asset preservation while ensuring continued healthcare coverage.

Pro tip: Consult an elder law attorney within 30 days of anticipating long-term care needs to develop a comprehensive asset protection strategy tailored to your specific financial situation.

Key Medicaid Eligibility and Look-Back Rules

Medicaid eligibility rules are complex financial regulations that determine an individual’s qualification for long-term care benefits. The primary criteria include strict income and asset limitations that require precise financial planning and strategic asset management. Families must navigate these intricate requirements carefully to preserve their resources while maintaining eligibility for critical healthcare support.

Medicaid Eligibility and Enrollment Rules demonstrate significant changes in how states evaluate and process healthcare coverage applications. The look-back period represents a crucial component of these rules, specifically a 60-month window during which all financial transfers are carefully scrutinized to prevent intentional asset sheltering.

Key eligibility considerations include:

Here’s a summary of major Medicaid eligibility factors and how they impact asset protection:

| Factor | Description | Impact on Family Assets |

|---|---|---|

| Income Limits | Restrictions on applicant’s monthly income | May require spend-down to qualify |

| Asset Thresholds | Maximum allowed asset value by state | Excess assets must be restructured |

| Exempt Resources | Assets not counted (home, car) | Certain items can be protected |

| Look-back Period | 60-month review of transfers | Non-compliant moves trigger penalties |

| Spousal Protections | Rules for non-applicant spouse | Allows retention of some assets |

- Asset thresholds vary by state

- Income limits determine initial qualification

- Certain assets are considered exempt (primary residence, personal vehicle)

- Transfers made during the look-back period can trigger significant penalties

- Spousal protections allow some asset preservation strategies

Professional elder law attorneys become essential in interpreting these complex regulations, helping families understand nuanced rules about asset transfers, exempt resources, and strategic financial restructuring that can protect family wealth while maintaining Medicaid eligibility.

Pro tip: Maintain meticulous financial documentation for at least 60 months prior to a Medicaid application to demonstrate transparent and compliant asset management.

Common Risks, Costly Mistakes, and Legal Issues

Medicaid crisis planning involves navigating a minefield of potential risks that can quickly derail financial protection strategies. Procedural errors and administrative oversights can transform a carefully crafted plan into a financial disaster, potentially leaving families vulnerable to catastrophic healthcare costs and asset loss.

Medicaid coverage risks demonstrate the complex landscape of potential legal challenges families face. Common mistakes include:

- Incomplete or incorrect documentation

- Misunderstanding asset transfer rules

- Failing to track look-back period transactions

- Improper use of asset protection trusts

- Overlooking state-specific eligibility requirements

The most significant legal pitfalls emerge from inadvertent violations of Medicaid regulations. Families can trigger severe penalties through seemingly minor mistakes, such as transferring assets below market value or failing to disclose complete financial information. Professional legal guidance becomes critical in preventing these costly errors that could result in months or even years of Medicaid ineligibility.

Understanding the nuanced landscape of Medicaid regulations requires a proactive approach. Each financial decision must be carefully evaluated against potential long-term consequences, with special attention to how asset transfers, income reporting, and estate planning intersect with Medicaid eligibility rules.

Pro tip: Create a comprehensive financial timeline and document every asset transfer at least 60 months before potential Medicaid application to minimize risk of penalties.

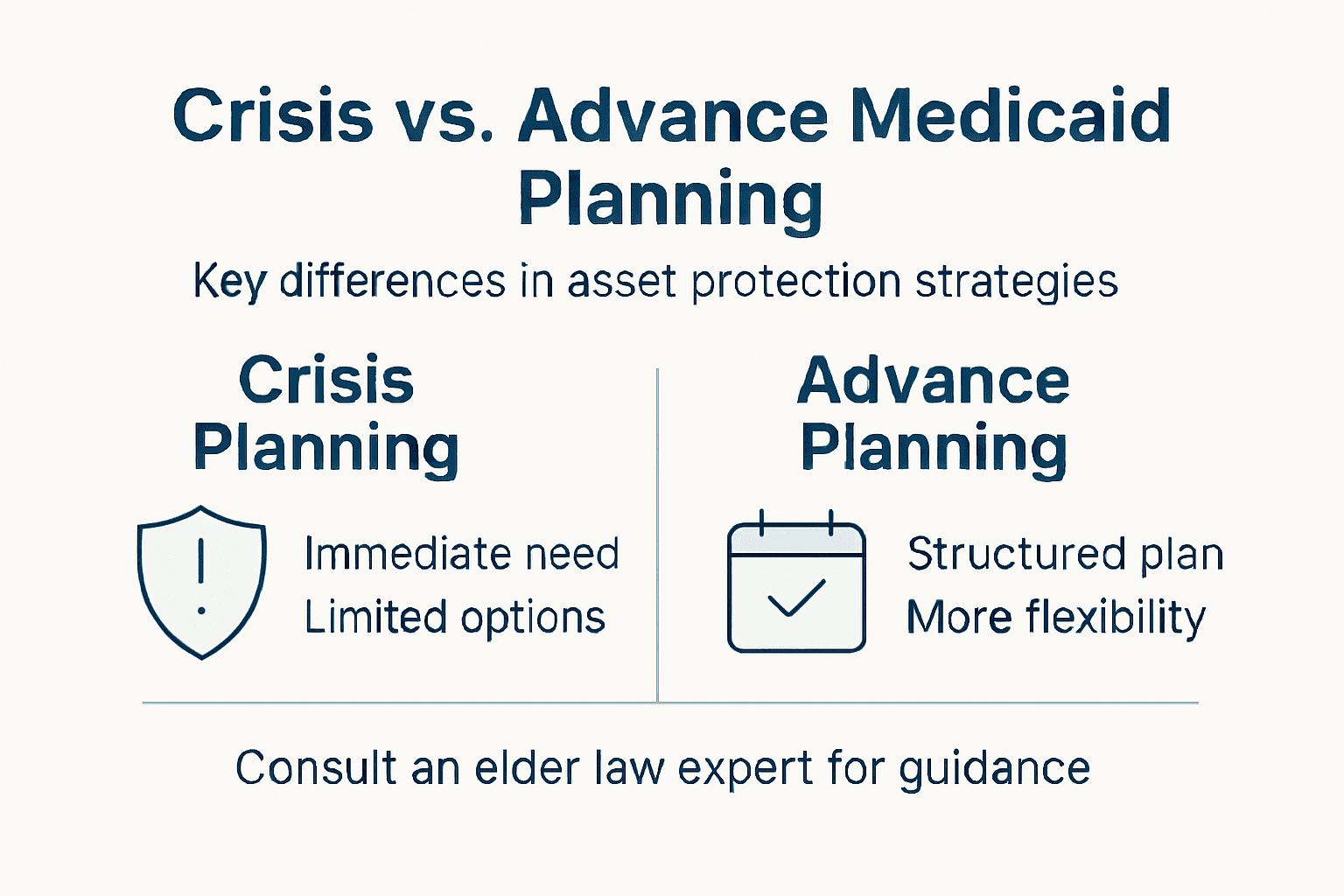

Comparing Crisis Planning With Advance Medicaid Strategies

Medicaid planning strategies fundamentally differ based on timing, with advance planning offering significantly more financial flexibility compared to urgent crisis interventions. Advance strategies allow families to methodically structure assets, create protective legal mechanisms, and anticipate potential long-term care needs well before immediate medical requirements arise.

Mobile crisis response strategies illustrate the critical differences between proactive and reactive approaches to healthcare and financial planning. The key distinctions include:

The table below outlines key differences between advance and crisis Medicaid planning:

| Planning Approach | Timeline | Asset Protection Options | Risk Level |

|---|---|---|---|

| Advance Planning | Years before care is needed | More strategies, flexible trusts | Lower risk of penalties |

| Crisis Planning | Immediate need for care | Limited strategies, urgent restructuring | Higher risk, less control |

-

Advance Planning:

- Comprehensive asset protection strategies

- Longer implementation timelines

- More legal and financial options

- Reduced risk of Medicaid penalties

-

Crisis Planning:

- Limited financial maneuverability

- Immediate, reactive decision-making

- Higher potential for asset loss

- Greater legal complexity

The most significant advantage of advance planning lies in its ability to create structured, legally sound asset protection mechanisms before urgent medical needs emerge. Families can strategically position resources, establish trusts, and navigate complex Medicaid regulations with minimal time pressure and maximum strategic control.

Pro tip: Start Medicaid planning discussions at least five years before potential long-term care needs to maximize financial protection and minimize legal complications.

Protect Your Family’s Future with Expert Crisis Medicaid Planning

Facing an immediate need for long-term care can bring overwhelming stress and confusion, especially when financial assets and Medicaid eligibility hang in the balance. The intricate rules around income limits, asset thresholds, and look-back periods make it crucial to act quickly and wisely. At Alatsas Law Firm, we understand the urgency of crisis Medicaid planning and the importance of preserving your family’s hard-earned assets under tight time constraints.

Our dedicated elder law attorneys specialize in navigating complex asset protection strategies such as irrevocable trusts and spend-down techniques to maximize Medicaid eligibility while safeguarding your wealth. Do not let rushed decisions lead to costly penalties that risk your financial security. Start with a clear path by exploring our comprehensive resources on elder law and Medicaid planning and schedule a personalized consultation. Act now to protect your assets and peace of mind—reach out through our contact page to secure the expert guidance your family deserves.

Frequently Asked Questions

What is crisis Medicaid planning?

Crisis Medicaid planning is an urgent legal strategy aimed at protecting a family’s financial assets when a senior requires immediate long-term care. It differs from traditional planning as it is executed under pressing circumstances where there is little time for preparation to qualify for Medicaid benefits.

When should a family consider crisis Medicaid planning?

Families should consider crisis Medicaid planning when a senior faces sudden health deterioration, unexpected medical diagnoses, or an immediate need for nursing home care, leaving limited time for strategic financial planning to protect assets and qualify for Medicaid.

What are some common strategies used in crisis Medicaid planning?

Common strategies include spousal asset transfers, establishing irrevocable trusts, implementing strategic spend-down techniques, and utilizing specific transfer mechanisms designed to preserve assets while complying with Medicaid regulations.

What are the risks associated with improper crisis Medicaid planning?

Improper crisis Medicaid planning can lead to significant penalties due to procedural errors, such as incomplete documentation or misunderstanding asset transfer rules. These mistakes can result in families losing crucial healthcare coverage and facing devastating financial consequences.