If you have ever asked, “how do i know which estate plan is right for me,” you are already doing the most important thing: pausing before making a costly mistake. In Brooklyn, we see middle-income families, caregivers, and small business owners try to “keep it simple” with a quick will, an online form, or a last-minute transfer of the house to the kids, then discover hidden taxes, probate delays, or Medicaid problems.

This guide translates legal options into everyday decisions, using a workshop-style process we use at Alatsas Law Firm. If you are juggling aging parents, a growing business, or a new chapter after divorce, this will help you choose a plan that actually works in real life. For a helpful starting point on organizing records, see Is Your Financial Information Up to Date?.

Ready to get clarity fast? Start the process with our guided intake: Schedule a Free Consultation.

Key Takeaways

- Estate planning is not “only for the wealthy”; the best estate plan for Brooklyn families often focuses on protecting a home, avoiding probate, and planning for long-term care.

- “How do i know which estate plan is right for me” starts with your risks; caregivers, business owners, and divorced parents need different protections.

- A will alone may not avoid probate; a properly funded trust can reduce court involvement and delays.

- Medicaid planning is time-sensitive; Brooklyn Medicaid planning strategies can protect assets when done early and correctly.

- Funding matters as much as documents; if accounts and deeds are not updated, the plan can fail when your family needs it most.

Understanding Estate Planning: What It Means for Brooklyn Families

Estate planning is a set of instructions and tools that protect your people and your property during life and after death. It is not just “who gets what.” In Brooklyn, the real-life goals are usually practical: keep the family home out of probate court, make sure someone can pay bills during a medical crisis, reduce family conflict, and preserve assets if long-term care becomes necessary.

A common scenario is a Bay Ridge couple who own a co-op, have a retirement account, and help a parent who is starting to forget medications. Their estate planning questions are not abstract. They are urgent: Who can talk to doctors? Who can access accounts if one spouse is hospitalized? What happens if the parent needs home care or a nursing home?

Why Brooklyn planning feels different than “generic” advice

Brooklyn families often have “one big asset,” the home, plus complex family dynamics. That could mean a brownstone in Bedford-Stuyvesant, a condo in Downtown Brooklyn, or a multi-family in Bensonhurst where relatives share space and expenses. Add blended families, adult children living at home, or a small business run from the ground floor, and the “simple will” approach can break down quickly.

Probate is also not just a legal process, it is a time and stress problem. According to the New York State Unified Court System, Surrogate’s Court is where probate matters are handled, and timelines vary widely depending on the estate and conflicts involved. You can review the court system’s overview here: New York State Unified Court System, Surrogate’s Court.

If you are wondering how do i know which estate plan is right for me, start by accepting this truth: estate planning is “life planning,” not a document purchase. Next, we will map your goals into a clear, step-by-step process.

How Do I Know Which Estate Plan Is Right for Me? A Step-by-Step Workshop Approach

The fastest way to answer “how do i know which estate plan is right for me” is to treat it like a workshop, not a transaction. In our experience, families make better decisions when they learn the rules first, then design the plan around real assets, real relationships, and real risks.

Here is the framework we use with Brooklyn families, small business owners, and caregivers.

Step 1: Name the “non-negotiables” (people, not paperwork)

Your plan should protect the people who depend on you. For a young professional, that might be a partner and aging parents. For a divorcing parent, it could be children and a co-parenting schedule. For a small business owner, it includes employees and a successor.

Ask: If you were unavailable for 60 days, who makes medical decisions and who pays the bills? That question often leads directly to the need for a Health Care Proxy and Power of Attorney. If you have an 18-year-old at home, read Coming of Age and Powers of Attorney because “adult” children create a surprising planning gap.

Step 2: Inventory what you have and how it transfers

The title on an asset controls what happens, even more than your will. A Brooklyn co-op shares, a home deed, a bank account with a beneficiary designation, and an LLC membership interest all transfer differently.

Use an estate planning to do list that includes:

- Identify every asset category (real estate, accounts, retirement, life insurance, business interests, valuables).

- Confirm how each item is owned (individual, joint, LLC, trust).

- Check beneficiary designations (many are outdated after marriage, divorce, or a death).

Step 3: Choose your “court involvement” level

One big divider in estate planning options explained is whether your family must go through probate. Some families accept probate if everything is straightforward. Others want to minimize it because of time, privacy, or blended-family tension.

If you are unsure whether a trust fits, this plain-English resource helps: When should a family consider a trust as part of an estate plan, and what type of trust should they use?.

Step 4: Stress-test for three Brooklyn-specific risks

The best estate plan for Brooklyn families is the one that survives real pressure. We stress-test for:

- A long-term care event that triggers Medicaid questions.

- A family conflict about “who gets the house” or who controls distributions.

- A business liability or lawsuit that threatens personal assets.

That stress-test naturally leads into the tools themselves, and why some “basic” plans are not truly basic in practice.

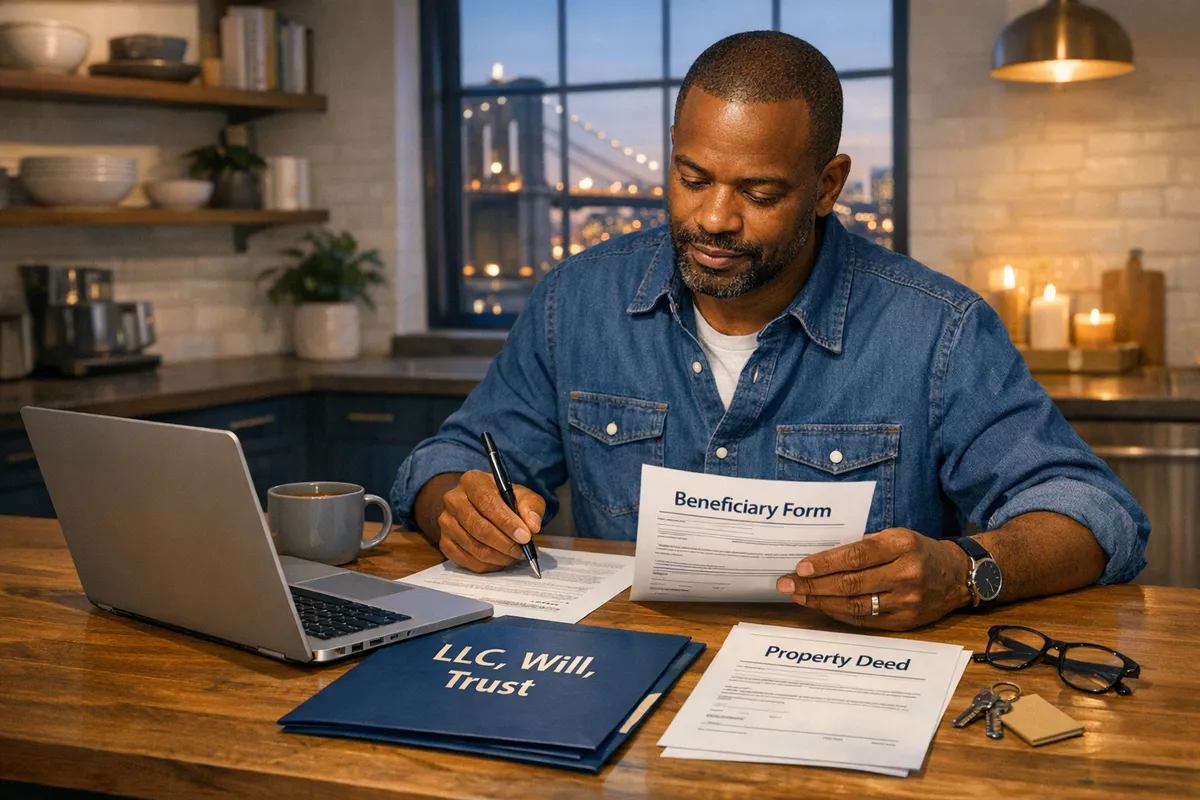

Estate Planning Options Explained: From Basic Wills to Complex Trusts

Estate planning options explained in plain English come down to control, timing, and protection. Most Brooklyn families do not need “fancy.” They need the right combination of documents that work together.

The “core five” documents many families start with

Think of these as your estate plan checklist for middle-income families. In many situations, you start with:

- Last Will and Testament to name executors and guardians, and to direct assets that do not pass by beneficiary.

- Power of Attorney to let a trusted person handle finances during life.

- Health Care Proxy to appoint a medical decision-maker.

- Living Will or advance directives to document medical wishes.

- HIPAA authorization so loved ones can access medical information.

For common questions about wills, see Last Wills and Testaments | Most Commonly Asked Questions.

When a trust is the “simple” solution, not the complex one

If your goal is probate avoidance or better control, a revocable living trust can be simpler for your family. It can also help with privacy, and it reduces the chance that one asset triggers a separate court process.

For many business owners, a trust also becomes the hub for succession planning, especially when paired with an LLC operating agreement and a clear plan for who can run the company during incapacity.

A warning about “easy fixes” like gifting the house to kids

Transferring your home during life can create tax and Medicaid problems you do not see coming. One of the biggest is losing the potential “step-up in basis,” which can increase capital gains taxes when children later sell. The IRS explains basis concepts here: IRS, Publication 551 (Basis of Assets).

So, if you keep asking how do i know which estate plan is right for me, consider this rule of thumb: if your plan changes the deed, changes beneficiaries, or changes ownership, you want legal guidance before you sign.

Next, we will talk about the planning issue that often drives urgency in Brooklyn: Medicaid and long-term care.

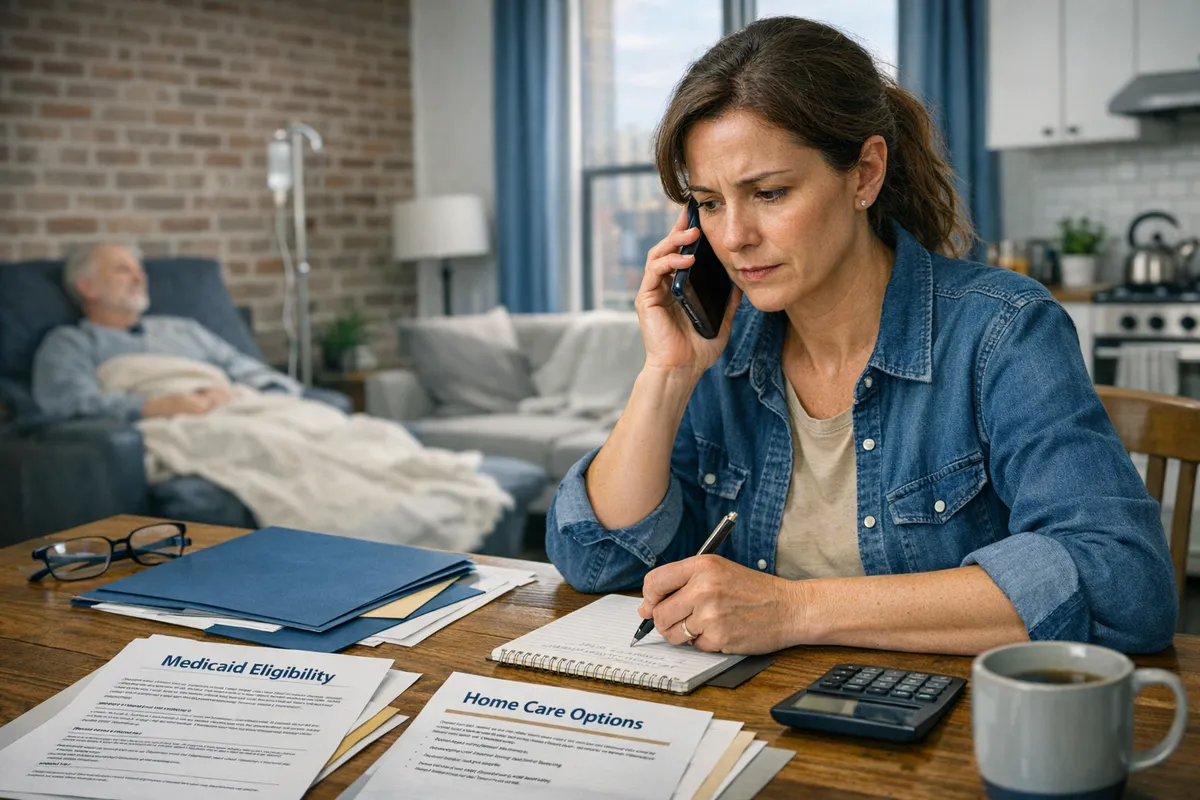

Medicaid and Asset Protection Strategies for Brooklyn Families

Brooklyn Medicaid planning strategies are not about “hiding money,” they are about avoiding preventable loss. Long-term care costs can rise quickly, and families often learn about Medicaid rules only after a hospital discharge planner says, “You may need nursing home placement.”

Start with what Medicaid does and does not cover in New York

Medicaid is a health coverage program, but the eligibility rules can affect your assets. Before making any transfers, learn the basics in What Medicaid Does (and Doesn’t) Cover in New York. For official program information, New York’s Medicaid page is here: New York State Department of Health, Medicaid.

A common caregiver scenario is an adult child in Midwood trying to keep a parent safe at home, while also worrying about the family home and a modest savings account. This is where planning timing matters.

The “timing” issue families miss

Many Medicaid planning tools depend on when you act. For example, Medicaid has rules around transfers, and the earlier a family plans, the more options they usually have.

When a crisis hits, retroactive benefits can sometimes help with immediate bills, but it is not a substitute for planning. If your family is already in crisis mode, read Using Retroactive Medicaid Benefits to Prevent Financial Disaster.

Asset protection tools that must be coordinated

The best estate plan for Brooklyn families often coordinates Medicaid planning with estate planning, not as separate projects. Depending on goals, tools may include an irrevocable trust designed for asset protection, careful beneficiary updates, and business structuring to separate personal and business risk.

If you are specifically thinking about the home, this resource explains common considerations: Should I put my primary residence in an irrevocable trust?.

If you are asking how do i know which estate plan is right for me, the Medicaid question is often the deciding factor. The wrong move can cause a penalty period or an unnecessary tax bill. The right move can protect a home, preserve dignity, and reduce family conflict.

Real Brooklyn Client Stories: How the Right Estate Plan Made All the Difference

The clearest way to understand how do i know which estate plan is right for me is to see what happens when a plan meets real life. Here are three anonymized examples that reflect what we commonly see at Alatsas Law Firm.

Story 1: The caregiver who avoided a forced sale

A daughter in Kensington was coordinating care for her mother after a fall. The family’s main asset was a two-family home, and the daughter feared it would have to be sold if her mother needed nursing home care.

By planning early and coordinating Medicaid strategy with the estate plan, the family protected the home and reduced conflict among siblings. The “win” was not just financial. It was the calm of having a clear plan and written authority to act when doctors and facilities needed answers.

For caregivers balancing stress and family dynamics, this is worth reading: 10 Strategies to Thriving as a Caregiver.

Story 2: The small business owner who separated business risk from family assets

A restaurant owner near Sheepshead Bay had an LLC but still had personal accounts and real estate exposed because beneficiary designations and ownership were never aligned with the bigger plan.

We updated the estate plan checklist for middle-income families to include business succession decisions, then aligned accounts and documents to match. The owner’s goal was simple: if something happens to me, my spouse can keep the business running and our home is not collateral damage.

Story 3: The divorced parent who prevented an “accidental” inheritance

A divorced parent in Park Slope had a will from before the divorce and a life insurance beneficiary that still named the ex-spouse. The client assumed the divorce “handled it.” It did not.

We redesigned the plan so the children were protected, guardianship language was clear, and the right people could manage funds responsibly. If you want to see how other clients describe the difference planning made, visit Testimonials From Our Family Law & Asset Protection Clients.

These stories share one theme: choosing the right plan is less about documents and more about designing a system your family can actually use.

Want a guided, workshop-style process instead of guesswork? Start your journey here: Start Your Journey.

Frequently Asked Questions About Choosing an Estate Plan in Brooklyn

What is the 5 by 5 rule in estate planning?

The “5 by 5 rule” is a common trust provision that lets a beneficiary withdraw the greater of $5,000 or 5% of trust principal each year, often to preserve certain tax advantages in older trust designs. Not every trust uses it, and many families never need it. If you see it in a document, ask your attorney what purpose it serves in your specific plan.

Can I create my own estate plan, or do I need an estate planning attorney?

You can create some documents on your own, but DIY plans often fail at ownership, beneficiary designations, and funding. In Brooklyn, the “gotchas” tend to be co-ops, multi-family homes, blended families, and Medicaid timing. If you are deciding how to choose an estate plan, an attorney can help you match tools to goals and prevent the expensive “fix it later” problem.

Your Next Steps: Put Your Plan in Motion

If you keep coming back to “how do i know which estate plan is right for me,” the answer is usually: the plan that protects your family during incapacity, minimizes avoidable court involvement, and accounts for long-term care risk. You do not need to be wealthy to need that protection. You just need to be realistic about what can happen.

Start by listing your assets, clarifying who you trust to act, and identifying whether Medicaid planning or business risk is part of your picture. Then work with local guidance to design and fund the plan, so it functions when it matters.

When you are ready, Alatsas Law Firm can help you move from uncertainty to a clear, practical plan that fits Brooklyn life.