If you own a business, care for a parent, or are rebuilding after divorce, your estate plan can quietly drift out of date without you noticing. The question “can an estate plan be updated regularly and how often” comes up constantly in our Brooklyn office, because life in New York moves fast, and the law does not wait for you to catch up.

The good news is that most estate plans can be reviewed and updated on a practical schedule, with “trigger events” that prompt immediate changes. This guide walks you through New York focused timelines, a step-by-step checklist, and what updating actually looks like for wills, trusts, and decision-making documents. For trust basics, see when to consider a trust and which type to use.

Ready to get organized without guesswork? Schedule a Free Consultation to review your current documents and update plan priorities.

Key Takeaways

- Review on a schedule and on life events; the right timing reduces surprises, delays, and family conflict.

- “Can an estate plan be updated regularly and how often” depends on change; big life, money, and health shifts should trigger immediate updates.

- New York execution rules matter; even “small edits” can backfire if done informally.

- Asset ownership and beneficiaries cause most failures; outdated titles and designations can override your will.

- A simple routine protects businesses and caregivers; you can plan for incapacity and succession before a crisis.

Understanding Why Regular Estate Plan Updates Are Essential in New York

In New York, an estate plan is not a one-time project, it is a living set of instructions that must match your current reality. When people ask can an estate plan be updated regularly and how often, what they are really asking is: “How do I keep my plan aligned with my family, my assets, and New York rules?”

A common Brooklyn scenario is a small business owner in Bay Ridge who formed an LLC, opened a new business bank account, and signed a commercial lease, but never updated their power of attorney or their trust funding. If something happens, the “right person” might not have clear authority to run payroll, access accounts, or negotiate a lease assignment. That is not a theoretical risk, it is a practical one.

New York-specific reasons updates matter

New York has its own probate process, Surrogate’s Court procedures, and property realities (co-ops, condos, multi-family homes). Even if your documents are valid, the way assets are titled often determines what happens.

For example, beneficiary designations on retirement accounts or life insurance typically control, even if your will says something different. The New York State Department of Financial Services explains how life insurance beneficiaries work and why keeping them current matters: NY DFS Life Insurance beneficiary basics). That is one reason “paper-only planning” fails.

If you are also trying to protect a home or savings from long-term care costs, updates are even more important. A plan that ignores Medicaid timing can create stress for caregivers who are already overwhelmed. For a broader view of how elder law planning fits in, read what an elder law attorney can do for you.

The bottom line is simple: a stale plan can be worse than no plan, because it creates false confidence. Next, let’s talk about realistic review timelines you can actually follow.

How Often Should You Review an Estate Plan? The 5 by 5 Rule and Beyond

A workable rule of thumb is to review your plan every 3 to 5 years, or within 3 to 5 months of a major change. That framework answers can an estate plan be updated regularly and how often in plain English, but it is not the whole story.

You may hear about the “5 by 5 rule” in estate planning. People use that phrase in different ways, but in everyday planning conversations it usually means: revisit your documents at least every five years, and sooner if any of five major categories change (family, money, health, tax, and where you live). Think of it as a memory aid, not a statute.

What “regularly” means for different Brooklyn households

For a young professional in Williamsburg with a basic will and health care proxy, a five-year review might be enough until the first major life event. For a middle-income caregiver in Bensonhurst coordinating a parent’s care, you may need more frequent check-ins because benefits, living arrangements, and decision-makers can shift quickly.

For small business owners, reviews tend to be more frequent because the business changes faster than personal life. If you added partners, signed a buy-sell agreement, or took on debt, it is time to review both your succession plan and your personal asset protection strategy.

A practical way to reduce overwhelm is to separate “review” from “rewrite.” A review can be a 30 to 60 minute check of:

- Who is in charge (executors, trustees, agents).

- What you own and how it is titled.

- Who receives what (beneficiaries, percentages).

If you want a prompt for the financial side, Is Your Financial Information Up to Date? is a helpful companion read.

To close the loop, regular reviews are also about reducing court involvement. The New York Courts website provides an overview of Surrogate’s Court functions, which helps families understand what probate and administration actually involve: NY Courts, Surrogate’s Court overview.

Now let’s get concrete: what changes should trigger an immediate update, even if you reviewed last year?

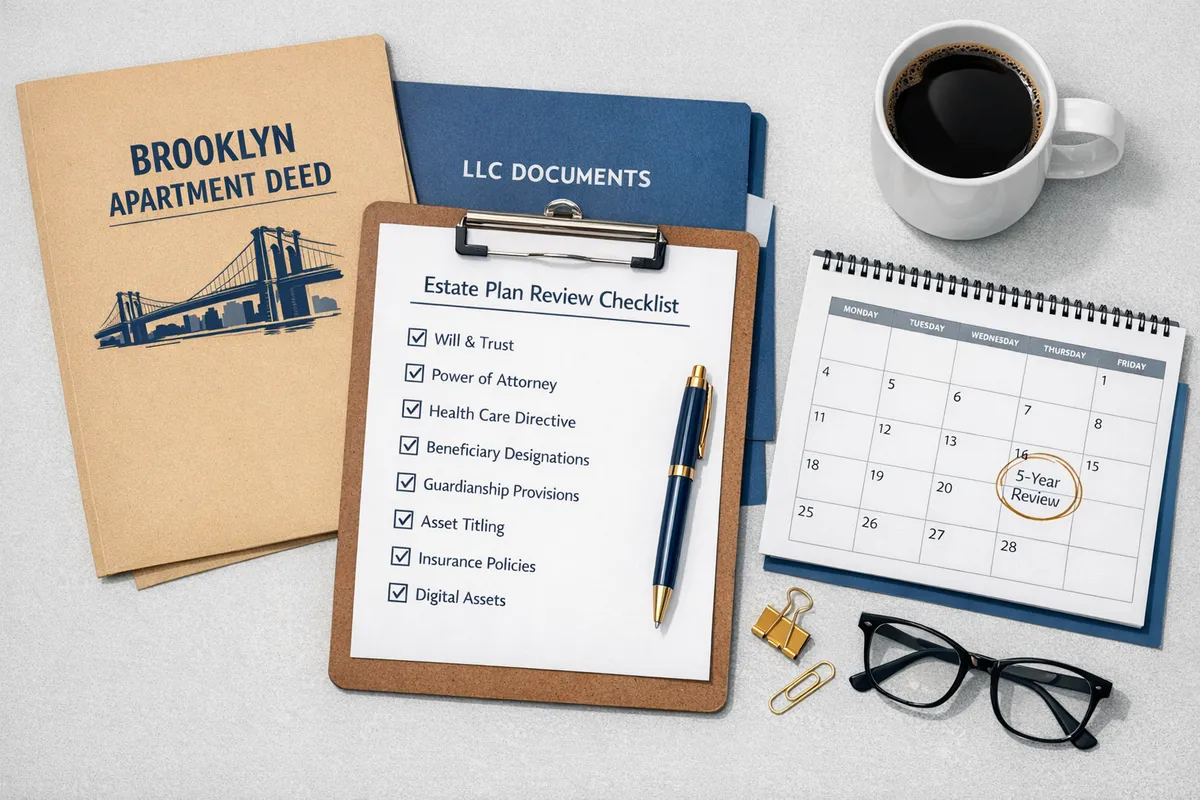

Key Signs You Need to Update Your Estate Plan: A Practical Checklist

If you want the simplest answer to can an estate plan be updated regularly and how often, it is this: update whenever your plan no longer matches your life. Below is an estate plan review checklist we use as a practical “trigger-event” tool for New York families.

The “update now” checklist (New York and Brooklyn realities)

- Marriage, divorce, or separation: New York rules and beneficiary designations do not automatically align with your intentions after a breakup. If family law issues are involved, updating is part of protecting your future.

- Birth, adoption, or guardianship changes: A will should name guardians for minor children, and a trust plan can control how money is managed until adulthood.

- A death, illness, or disability in the family: If your executor, trustee, or agent is no longer able to serve, your plan needs new decision-makers.

- Move within NYC or out of state: Even within NYC, property types differ. Co-op transfers and house titles can change how planning works.

- Buying or selling real estate: A new property often means new deeds, new insurance, and new funding steps for trusts.

- Big asset changes: Selling a business, adding a partner, receiving an inheritance, or significant retirement account growth can change tax and distribution planning.

- New business risk: If you signed personal guarantees, expanded payroll, or shifted from sole proprietor to LLC, you may need asset protection updates.

- Long-term care concerns: If a parent is declining, timing matters. Waiting too long can limit options.

- Your “personal property story” changed: Families fight over sentimental items, not just money. If you have heirlooms, collections, or specific wishes, document them.

In our experience, the most overlooked trigger is personal property. Someone in Park Slope may have a modest estate, but a lifetime of “memory makers” in jewelry, art, or family religious items. Writing those wishes down can prevent conflict. See Memory Makers: Your Personal Possessions for a simple approach.

A quick example: the “good plan, bad timing” problem

Consider a divorcing parent in Flatbush who updated a will, but forgot to change retirement account beneficiaries and a life insurance policy. If they die unexpectedly, those beneficiary forms can override the will, creating the exact outcome they were trying to prevent.

If you are thinking, “This sounds like me,” that is not a reason to panic. It is a reason to take the next section seriously, because New York has formal requirements for changing documents.

Updating Wills and Trusts in New York: Legal Steps and Brooklyn Estate Planning Update Rules

Updating wills and trusts in New York is absolutely doable, but it must be done with the same formality as the original signing. When clients ask can an estate plan be updated regularly and how often, they also need to know the “how,” so they do not accidentally create a contest or an invalid document.

For wills, changes are typically made by:

- A codicil (an amendment to a will) that is properly executed, or

- A new will that revokes the old one.

In practice, many attorneys prefer a new will if there are multiple changes, because it is cleaner and reduces confusion.

For trusts, the answer depends on the type. Revocable living trusts are commonly amended during life, while irrevocable trusts are harder to change and often require specific legal pathways. If you are considering placing your home into an irrevocable trust, read Should I put my primary residence in an irrevocable trust?.

“Brooklyn estate planning update rules” also includes the practical reality of execution: witnesses, notarization where appropriate, and consistent paperwork across banks, brokerages, and title companies. Handwritten edits in the margin are a common mistake. They feel efficient, but they can create real litigation risk later.

Next, let’s turn this into a repeatable routine, so you are not reinventing the wheel every few years.

Creating a Sustainable Estate Plan Update Routine to Protect Your Legacy

The best estate plans get updated because the family has a system, not because they got lucky. If you have been wondering can an estate plan be updated regularly and how often without it turning into a stressful project, the answer is yes, if you build a simple cadence.

A realistic routine for busy New Yorkers

Start with two calendar dates:

- Annual “admin day” (30 minutes): Confirm addresses, passwords storage, and decision-makers. Check beneficiary designations on retirement accounts and life insurance.

- 3 to 5-year legal review (60 to 90 minutes): Review your will, trust terms, and incapacity documents with counsel.

Then add a “trigger rule”: if any major life event occurs (marriage, divorce, birth, death, business sale, major diagnosis), schedule a review within 90 days.

A small business owner example: you open a second location and take on a business partner. That is a perfect time to re-check your powers of attorney, your trust funding, and your business succession documents. It is also when asset protection becomes practical, not abstract.

If you do not have close family or your chosen beneficiaries may change, updates matter even more. Plans for people without heirs often include charities, friends, or more detailed fiduciary choices. See Estate Planning With No Heirs for planning ideas that prevent the “default to distant relatives” outcome.

Want a guided, step-by-step process instead of piecing it together? Start your journey with Alatsas Law Firm using Start Your Journey, and we will help you prioritize updates that match your family and your assets.

A sustainable routine is also about communication. Tell your executor or trustee where documents are stored, and keep a secure list of accounts. If you need help choosing the right legal roles, Appointing legal representation and what you need to know explains the decision in plain English.

Up next: quick answers to the most searched questions we hear every week.

Frequently Asked Questions About Estate Plan Reviews in New York

How often should an estate plan be reviewed?

Most people should review an estate plan every 3 to 5 years, and immediately after major life events like marriage, divorce, a birth, a death, a business sale, or a serious diagnosis. In New York, changes in asset ownership and beneficiary designations are also review triggers, because they can control transfers outside of your will. A short review is often enough to catch problems before they become expensive.

What is the 5 by 5 rule in estate planning?

The “5 by 5 rule” is a practical reminder to revisit your plan at least every five years, and sooner when key areas of your life change. People use the phrase differently, but the spirit is consistent: do not let documents sit untouched for a decade. For families with businesses, blended families, or elder care needs, the “sooner” part matters most.

Can an estate plan be updated regularly and how often without creating legal problems?

Yes, an estate plan can be updated regularly, as long as updates are done correctly and consistently across documents and accounts. The safest approach is to treat updates like formal legal work, not casual edits. That means proper execution, clear revocation language when replacing documents, and coordination with titles and beneficiaries. A routine review schedule plus trigger-event updates is usually the best balance.

Your Next Steps for a Plan That Stays Current

Regular reviews are how you keep your plan protective, not just “on file.” If you have been asking can an estate plan be updated regularly and how often, aim for a 3 to 5-year legal review, plus quick check-ins after major changes.

New York families are busy, and Brooklyn life comes with unique property, business, and caregiving pressures. The right routine reduces probate risk, keeps decision-making authority clear, and helps your loved ones avoid confusion when they need clarity most.

If you are unsure where to start, begin with one step: gather your documents and list your assets, then talk with an attorney about what actually needs to change now versus later.