If your Brooklyn family business is your retirement plan, your kids’ inheritance, and your safety net, one lawsuit or rushed handoff can put all three at risk. Using Trusts to Transition Family Businesses Without Losing Asset Protection is often the difference between a smooth succession and a preventable financial hit for the whole family.

I have seen owners in neighborhoods like Bay Ridge, Bensonhurst, and Williamsburg do “handshake” transitions that looked simple, until creditors, taxes, or family conflict showed up. This article breaks down practical trust-based strategies, in plain English, so you can protect what you built. For a primer on when a trust belongs in an estate plan, start here: When should a family consider a trust as part of an estate plan, and what type of trust should they use?

Ready to protect your business and your family’s assets? Schedule a Free Consultation and we will map out the safest next steps.

Key Takeaways

- Succession is also liability planning: A “successful” transition is one that limits creditor exposure and family conflict.

- Irrevocable trusts can protect personal wealth: Properly structured irrevocable trusts in New York can shield assets while supporting family goals.

- Using Trusts to Transition Family Businesses Without Losing Asset Protection takes coordination: The trust, the LLC/corporation, and your operating documents must work together.

- Middle-income families benefit too: Asset protection trusts for small businesses are not only for the ultra-wealthy.

- Funding and administration matter: A trust that is never funded, or is run loosely, often fails when tested.

Why Family Business Succession Planning in Brooklyn Needs Trust-Based Strategies

Brooklyn succession planning is rarely just about who gets the keys, it is about keeping family assets intact while control changes hands. In our experience at Alatsas Law Firm, many small-to-midsize owners have two intertwined balance sheets: the business and the household. When those lines blur, a business problem becomes a personal crisis.

A common scenario is a second-generation owner taking over a storefront business while the parents keep signing leases or personally guaranteeing credit lines. If a vendor dispute turns into a judgment, plaintiffs look for deep pockets, and personal guarantees can expose savings, home equity, and even college funds.

What makes Brooklyn transitions uniquely tricky

Real estate and leases are high-stakes here. Commercial rent in neighborhoods like Downtown Brooklyn or Park Slope can force owners to sign long leases, and landlords often require personal guarantees. Add dense customer traffic, delivery accidents, and employee issues, and liability risk is not theoretical.

Family dynamics also show up fast. One child works in the business, another does not, and a third is caregiving for a parent. Without a structure, “fair” can become a fight. Trust-based family business transition strategies can create a clear lane for decision-making and distributions, instead of leaving everyone to argue under pressure.

Finally, succession is connected to elder law more often than families expect. If long-term care becomes part of the picture, planning needs to consider asset protection and benefit eligibility. If you are weighing that overlap, this background helps: Elder Law Attorneys and What They Do.

The good news is that trusts can help separate business risk from personal wealth, while still allowing an orderly handoff.

Understanding Trust Structures: Irrevocable Trusts and Asset Protection Trusts in New York

Not all trusts protect assets, and not all asset protection tools fit a Brooklyn business owner’s reality. When people hear “trust,” they often think of a revocable living trust. That can be great for avoiding probate, but it typically does not protect assets from creditors because you can revoke it and pull assets back.

For Using Trusts to Transition Family Businesses Without Losing Asset Protection, two categories come up most often: irrevocable trusts and asset protection trusts.

Irrevocable trusts in New York (plain-English version)

With an irrevocable trust, you generally give up some control in exchange for protection. The trust becomes the legal owner of the assets you transfer into it, and a trustee manages those assets under written rules.

For many middle-income families, the most relatable asset is the home. A properly designed plan can help protect a residence while still allowing the parent to live there, but it must be done correctly. If you are thinking about placing a home into a trust, read this first: Should I put my primary residence in an irrevocable trust?

A business interest can sometimes be transferred too, but we usually coordinate that with the company’s operating agreement, buy-sell provisions, and lender requirements.

Asset protection trusts for small businesses: what people mean

When clients ask about “asset protection trusts,” they often mean a structure designed to make it harder for creditors to reach assets, while still benefiting a spouse, children, or future generations. In New York, you cannot simply create a “magic” self-settled trust that blocks all creditors in every situation. The details matter, including who the beneficiaries are, who serves as trustee, and the timing and purpose of transfers.

You also have to coordinate with entity planning. An LLC can limit liability for business operations, but it does not automatically protect your personal assets if you personally guarantee debts or co-mingle funds. For an official overview of New York LLC formation basics, see the New York Department of State: Limited Liability Companies.

If you are going to build a trust-based plan, accuracy matters. Outdated beneficiary designations, missing account statements, or wrong ownership titles can quietly undermine the whole strategy. This checklist-style reminder is helpful: Is Your Financial Information Up to Date?.

Next, let’s turn these concepts into a practical, four-step playbook.

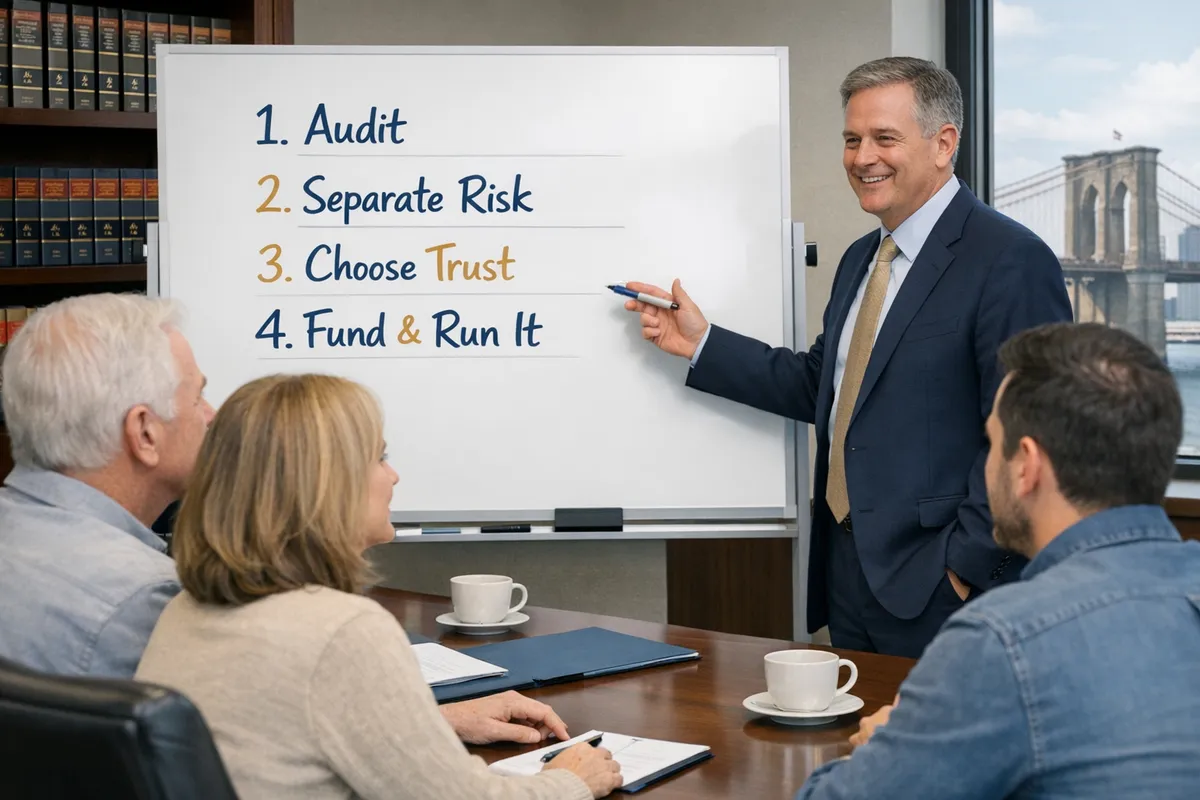

A Four-Step Trust-Based Playbook for Transitioning Your Family Business Without Losing Asset Protection

A protected transition is built, not wished into existence, and it usually follows a clear sequence. The goal is to transfer value and responsibility without accidentally transferring liability to the next generation, or exposing the parents’ nest egg.

Step 1: Audit what you own, and how it is titled

Start with a “who owns what” snapshot: business shares or membership interests, real estate, bank accounts, vehicles, equipment, and intellectual property. Then identify where the risk is. Are there personal guarantees? Are there co-owned accounts with adult children? A surprising number of transitions fail because the paperwork does not match the family’s assumptions.

This step also reveals whether you need coordination with family law planning. For example, if an adult child taking over the business is divorcing, you may need to consider how ownership is documented and protected.

Step 2: Separate operating risk from family wealth

This is where entity planning and trust planning meet. We often look at whether the business should be in an LLC or corporation, how leases are signed, and whether family real estate should be held outside the operating entity.

For many owners, the “aha” moment is realizing that asset protection is layered. An LLC is one layer, and a trust can be another. Neither replaces the other.

Step 3: Use the right trust for the right job

Using Trusts to Transition Family Businesses Without Losing Asset Protection usually means matching the trust to the asset and the family’s timeline. Examples include:

- Irrevocable trusts for legacy assets like a residence or a long-held investment account, where you want creditor protection and smoother transfer.

- Trust ownership of business interests where appropriate, often paired with rules that prevent an in-law from gaining control and that set standards for distributions.

Gift and transfer rules can also matter if you are shifting ownership to children or to a trust. The IRS overview is a reliable place to start for federal gift tax basics: Gift Tax.

Step 4: Fund the trust and run it like you mean it

A trust that is not funded is mostly paper. Funding can include retitling accounts, assigning membership interests, updating beneficiary designations, and documenting trustee powers.

Then comes administration. Keep clean records, follow distribution rules, and avoid treating trust assets like an informal piggy bank. The trust must be respected to be respected. If probate avoidance is also part of your goal, we can help you understand how trusts and court processes differ. The New York courts provide a general overview here: Surrogate’s Court procedures.

Once you have the structure, the next step is making sure common myths do not push you into shortcuts.

How to Protect Family Assets During Business Transition: Overcoming Common Misconceptions

The biggest threat to asset protection is usually not a creditor, it is a confident misunderstanding. When families are stressed, they gravitate toward “simple” solutions that create expensive consequences later.

One misconception is that trusts are only for wealthy families. In reality, many Brooklyn owners are “asset rich, cash tight.” A paid-off home, a modest retirement account, and a business that supports the household is worth protecting.

Another misconception is that “I can just put everything in a trust and I am safe.” Using Trusts to Transition Family Businesses Without Losing Asset Protection requires proper timing, proper drafting, and proper funding. Transfers made when a lawsuit is already brewing can be challenged, and sloppy administration can weaken the protections you thought you had.

Finally, some owners assume their accountant or insurance broker “has it covered.” Those professionals are crucial, but the legal structure still needs an attorney who does this work regularly. If you are wondering what that legal guidance can look like, this is a good starting point: What Are The Benefits of Hiring an Elder Law Attorney?.

Brooklyn Case Study: A Successful Trust-Based Family Business Transition

Picture this: a family sits in our Sheepshead Bay office, holding a lease renewal and a stack of personal guarantee forms they did not fully understand. The parents owned a small distribution business serving restaurants across Brooklyn and Queens. Their adult daughter ran day-to-day operations, and their son handled deliveries. The parents wanted to step back, but they were worried about protecting the home and savings they needed for retirement.

Here is what we did, in a simplified (and anonymized) version of the plan. First, we reviewed the entity structure, guarantees, and how accounts were titled. Then we built trust-based family business transition strategies that separated operating risk from family wealth, including using an irrevocable trust for certain personal assets and clear successor management rules for the business.

We also added “human” protections: who can sign contracts, what happens if one child wants out, and how disputes get resolved. Clarity reduced conflict as much as it reduced liability.

The outcome was a transition that kept operations stable while creating stronger asset protection boundaries. Just as important, the family felt confident because they understood the plan in plain English, and they had a system for keeping it updated.

If you want to hear how we think through asset protection planning in real life, this is a helpful companion resource.

Want to keep learning without the jargon? Listen to our audio resource: Listen Now.

Frequently Asked Questions About Trusts and Family Business Transitions

Should I put my family business in a trust?

Sometimes, but not automatically. Putting a family business in a trust can support continuity, protect a child from outside claims, and create clear rules for governance, but it has to match your operating agreement, lender requirements, and tax strategy. In many plans, we place business interests in a trust while keeping day-to-day control with the right manager, and we keep certain operating assets outside the trust to preserve flexibility.

Will a family trust protect my assets?

A trust can protect assets, but only the right kind of trust, funded and administered correctly. A revocable living trust usually helps with probate avoidance, not creditor protection. For asset protection, families often explore irrevocable trusts in New York, where the trust truly owns the assets and the trustee follows strict rules. Using Trusts to Transition Family Businesses Without Losing Asset Protection works best when the trust is coordinated with entity planning and clean financial habits.

Your Next Steps for a Safer Transition

A family business transition should not require you to gamble your home, your retirement, or your peace of mind. The most effective plans use layered protection: solid business entities, smart contracts, and carefully chosen trusts.

If you are considering Using Trusts to Transition Family Businesses Without Losing Asset Protection, start by gathering accurate ownership documents and identifying where personal guarantees or co-mingled finances create exposure. Then get guidance that fits Brooklyn families and real-world budgets.

For examples of how clients describe our approach, you can read Testimonials From Our Family Law & Asset Protection Clients. When you are ready, we will help you build a plan you can actually understand and maintain.