If you assume your stepchild will “automatically” inherit, you may be betting your family’s future on a rule that does not exist. Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents are often limited without the right documents, especially in blended families where prior marriages, new spouses, and beneficiary designations collide.

Whether you are a Brooklyn small business owner protecting assets, a caregiver trying to keep peace at home, or a divorcing parent seeking clarity, this guide breaks down what stepchildren typically do (and do not) receive under the law, and how to lock in your wishes with practical steps. For a will refresher, see Last Wills and Testaments: Most Commonly Asked Questions.

Ready to get a plan on paper? Schedule a Free Consultation with Alatsas Law Firm to talk through options for your blended family.

Key Takeaways

- Stepchildren usually do not inherit by default — stepchildren inheritance laws often exclude them under intestacy unless they are legally adopted or specifically named.

- Beneficiary forms can override your will — retirement accounts and life insurance pay by designation, not by your probate plan.

- Trusts add structure and protection — trusts for stepchildren and dependents can reduce conflict and control timing, spending, and creditor exposure.

- Clarity prevents litigation — a clean paper trail reduces the chance someone argues “undue influence” or a mistake.

- Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents are customizable — but only if you actively plan, update, and coordinate documents.

Understanding Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents

Here is the hard truth: in many families, “love and time raised them” does not equal legal inheritance. Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents depend on state law, marital status at death, and whether you took steps to legally include them.

In New York, if someone dies without a will (called “intestacy”), the statute generally prioritizes a surviving spouse and biological or legally adopted children. Stepchildren are commonly left out unless adopted. The New York courts’ plain-English overview is helpful: NY Courts: Intestacy. That is why families in Sheepshead Bay, Bay Ridge, and across Brooklyn get blindsided after a death, even when everyone “knew” the stepparent wanted the stepchild treated equally.

Why blended families get hit harder than they expect

The biggest risk is the “accidental disinheritance” created by default rules. A common scenario is a second marriage where one spouse assumes the other will “take care of the kids.” Legally, the surviving spouse may inherit first, and then leave everything to their own children later. Your stepchild can end up with nothing, even if the relationship was loving.

Non-biological dependents face similar issues. If you are raising a grandchild, supporting a partner’s child, or caring for a niece, the legal rights of non-biological dependents are usually not automatic. The law tends to reward formal relationships, not caregiving history.

This reality is not meant to scare you. It is meant to move you from assumptions to documents, which is where the next section goes.

Key legal tools for including stepchildren in your estate plan

The fastest way to protect a stepchild is to name them clearly and coordinate every place money can transfer. Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents are built with a few core tools, but they have to work together.

Wills: how to include stepchildren in a will (and avoid ambiguity)

A will is still the foundation for many families, especially when you need guardianship nominations for minor children and a clear statement of intent. If your goal is “treat all kids equally,” your will must say who “kids” are. Use full legal names, relationships, and alternates.

Two practical drafting tips reduce conflict: first, define whether “children” includes stepchildren; second, include a no-contest clause where appropriate (your attorney will explain limits under New York law). If you want a deeper look at when a will is not enough, see When should a family consider a trust as part of an estate plan, and what type of trust should they use?.

Trusts: control timing, protect from creditors, and reduce second-marriage risk

Trusts for stepchildren and dependents can solve the “surviving spouse dilemma.” For example, a trust can allow a surviving spouse to live in the home or receive income, while preserving the principal for your stepchildren and your biological children. That is often the fairest approach in estate planning for blended families.

Trusts also matter for business owners. If you have an LLC interest, customer contracts, or equipment, a trust-based plan can help manage succession and keep assets from being mishandled during probate.

Beneficiary designations: the silent estate plan that overrides the loud one

Retirement accounts, life insurance, and many bank accounts transfer by beneficiary form. A beneficiary designation can defeat your will in one signature. In our experience, the biggest “stepchild mistake” is leaving a 401(k) to “spouse” and assuming the spouse will later “share.” Sometimes they do. Sometimes they cannot, or do not.

If you have not checked your forms recently, start with Is Your Financial Information Up to Date?. Then confirm contingent beneficiaries, per-stirpes language, and whether minors need a trust as beneficiary.

These tools get powerful when you apply them in a repeatable process, which is what the checklist section is for.

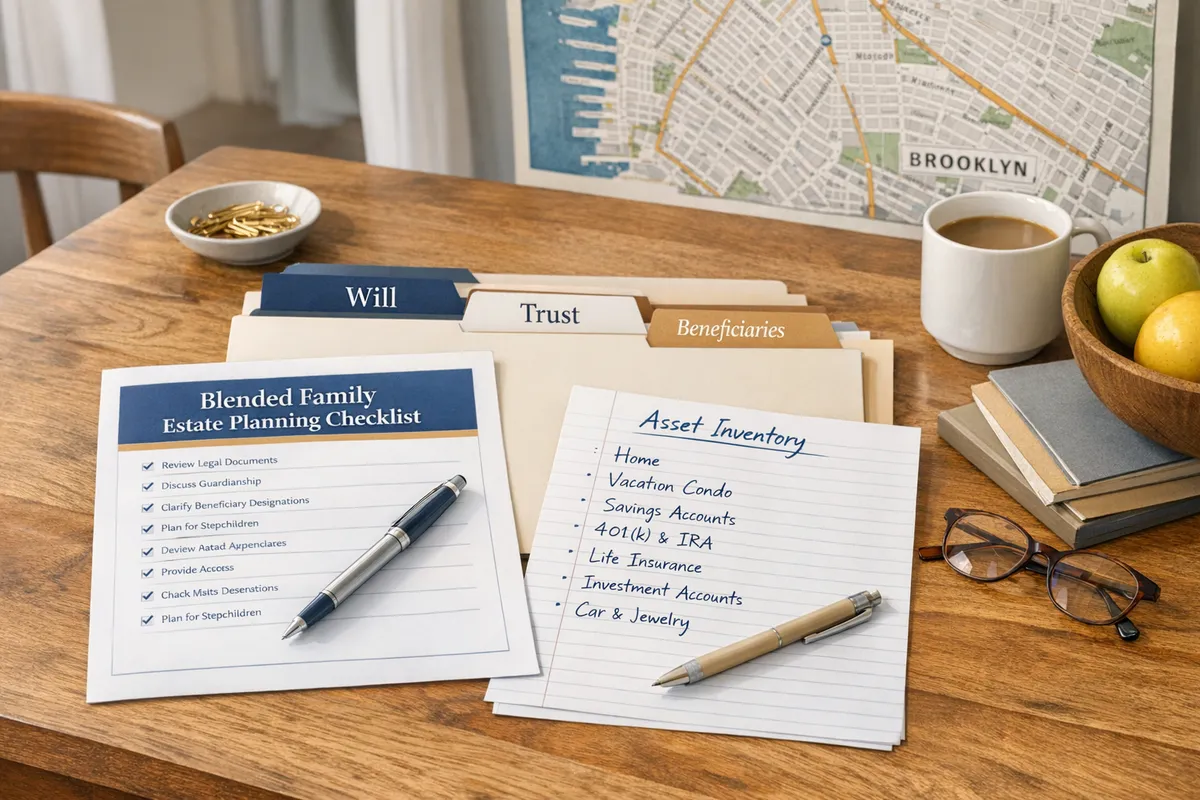

Step-by-step estate planning checklist for blended families

A blended-family plan works best when you treat it like a project, not a single document. This checklist is a locally-tested framework our Brooklyn clients use to turn Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents into real-world outcomes.

The “Brooklyn Blended Family” checklist you can start this week

- Map the family in writing. List each spouse, ex-spouse, child, stepchild, and any non-biological dependent you support, plus who should receive what and when. This reduces “I thought you meant…” disputes.

- Inventory assets by transfer method. Separate “probate assets” (often controlled by a will) from “non-probate assets” (beneficiary designations, joint accounts, transfer-on-death). The split is where most surprises happen.

- Check title and ownership on the big-ticket items. Your home, co-op shares, and business interests may have ownership structures that control who inherits. If you are a business owner, confirm operating agreements and succession language.

- Choose your protection strategy. Decide if a will alone is enough or if you need a trust, such as a marital trust plus a separate trust for children from a prior relationship.

- Coordinate beneficiary forms with the plan. Update retirement accounts, life insurance, and payable-on-death accounts so they match your intent for stepchildren and dependents.

- Plan for incapacity, not just death. Powers of attorney and health care proxies matter when family dynamics are complicated. For more on selecting the right decision-makers, read Appointing Legal Representation and What You Need To Know.

A quick template for “fair, not equal” distributions

Fair does not always mean equal in blended families. For example, you might leave the business interest to the child working in the business, while using life insurance or a trust to provide an equivalent inheritance to a stepchild who is not involved. The key is documenting the reasoning in the plan so it feels intentional, not punitive.

If sentimental property is part of the tension, create a personal property memorandum and talk it through early. Start with Memory Makers: Your Personal Possessions.

Once you have the checklist, the next question is how it plays out in real life. The case study below shows how small updates can prevent big losses.

Case study: how trusts and beneficiary updates protected a blended family’s legacy

One beneficiary update can be the difference between “smooth transfer” and a family split that lasts for years. Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents become real when money and emotions hit at the same time.

A Brooklyn small business owner remarried and helped raise his wife’s daughter from middle school through college. He also had one adult son from his first marriage. His “plan” was a simple will and the expectation that his spouse would “do the right thing.”

We reworked the plan into a trust that provided for the spouse’s housing needs while preserving a defined share for both kids. Then we updated his life insurance and IRA beneficiaries to match the trust design. When he died unexpectedly, the accounts paid out exactly as intended, without probate delays or second-marriage tension. Both children received support, and the surviving spouse had stability.

Future-proofing your estate plan: practical tips to safeguard stepchildren’s interests

Most estate plans fail because they get stale. Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents are not “set it and forget it,” especially when remarriage, divorce, business growth, and caregiving change your risk profile.

Update triggers you should treat as non-negotiable

Review your plan after any major life event, including remarriage, divorce filings, a new child, buying a home, selling a business, or a serious diagnosis. For divorcing parents, it is also critical to coordinate your estate plan with separation agreements and support obligations so the documents do not contradict each other.

State-by-state rules vary, and online searches like “Do stepchildren have inheritance rights in California?” or “Do stepchildren have inheritance rights in Texas?” often surface because families move. If you relocated to or from New York, re-check your documents with local counsel. Florida’s homestead rules, for example, can produce very different outcomes than New York.

Protecting inheritances from taxes, creditors, and caregiving costs

Business owners often worry about lawsuits and creditor exposure. A properly structured trust can add layers of protection for an heir, including a stepchild, who is young, financially inexperienced, or in a high-liability profession.

Caregivers have a different fear: long-term care costs. While Medicaid planning is its own topic, you should understand that transferring assets incorrectly can backfire. If your family includes a dependent with disabilities, consider whether an ABLE account or special needs trust is appropriate. This guide helps clarify options: ABLE versus Special Needs Trust: What Works for You?.

Document the “why,” not just the “what”

A short letter of intent can lower the temperature in a blended-family estate. It is not a legal document, but it explains your reasoning and your hopes. That matters when someone is grieving and reading numbers on a page.

For tax basics, it also helps to understand stepped-up basis for inherited assets. The IRS explains basis rules here: IRS Publication 551.

When you combine updates, protections, and clear communication, you are not just “including” a stepchild. You are building a plan that can survive real life.

Frequently asked questions about stepchildren inheritance laws

Can I leave my stepchildren nothing if my husband dies?

Yes, in many situations a stepchild can receive nothing unless you name them, especially if you die without documents or your assets pass to your spouse first. The bigger issue is what happens after your spouse inherits. Your spouse can usually change their own will later, and their plan may favor their biological relatives. If you want your stepchildren protected, name them directly and consider a trust that controls what happens after the surviving spouse’s lifetime.

Are stepchildren entitled to inheritance?

Usually no, stepchildren are not automatically entitled to inherit under intestacy rules, unless they were legally adopted or covered by a specific statute in your state. That is why “we were close” is not a legal strategy. If your goal is to provide for a stepchild or other non-biological dependent, you typically need a will, trust, and coordinated beneficiary designations that clearly identify them.

How does inheritance work with stepchildren?

Inheritance for stepchildren usually works only if you proactively create it, either by naming them in a will or trust, adopting them, or designating them on beneficiary forms. Many assets, like life insurance and retirement accounts, transfer outside probate and will follow the beneficiary paperwork even if your will says something else. A coordinated plan is what turns intent into enforceable outcomes.

Your next steps for protecting the people you raised and love

A blended family can be beautifully close, and legally fragile at the same time. The fix is not complicated, but it does require follow-through: clarify your intent, choose the right mix of will, trust, and beneficiary updates, and then keep the plan current.

If you take one idea from this guide, make it this: Inheritance Rights and Protections for Stepchildren and Non-Biological Dependents are created by planning, not assumptions. When your documents match your real family, you reduce conflict and protect everyone’s dignity.

If you are ready for a practical plan tailored to Brooklyn families, Alatsas Law Firm can help you put the right protections in place and keep them updated as life changes.