If you have ever watched a family wait months (sometimes longer) for Surrogate’s Court to approve basic paperwork, you already understand why avoiding probate in New York matters. In my Brooklyn practice, I see it hit everyone, the small business owner trying to keep the company running, the caregiver juggling a parent’s bills, and the young professional who just wants things to be simple.

Avoiding probate in New York is not about hiding assets or cutting corners. It is about using the right legal tools, and then actually “funding” them correctly, so your family can access money and transfer property without a court process. For a deeper overview of core planning documents, see Five Documents Needed for Estate Planning in NY.

Start your plan with clarity. If you want a step-by-step process for avoiding probate court in New York, Schedule a Free Consultation.

Key Takeaways

- Probate is a court process that can slow down access to accounts and real estate, even in organized families.

- Avoiding probate in New York usually means using ownership and beneficiary tools, not just a will.

- A revocable living trust only works if it is funded, meaning assets are retitled into the trust.

- Joint ownership can backfire if it creates creditor exposure, family conflict, or tax issues.

- Good planning is maintenance, so updates after life changes keep your strategy intact.

Understanding Probate and Why Avoiding Probate in New York Matters

Probate is the court-supervised process of proving a will and appointing an executor. In New York, that typically happens in Surrogate’s Court under rules found in the SCPA (Surrogate’s Court Procedure Act) and property transfer concepts in the EPTL (Estates, Powers and Trusts Law). If there is no will, the family may need an “administration” proceeding instead, and New York’s intestacy rules decide who inherits.

Families often tell me, “We have a will, so we are covered.” A will is essential, but it is also a ticket into court. A will does not avoid probate, it directs probate. That distinction matters when your spouse needs immediate access to funds, or when a caregiver child is already stretched thin.

What probate can cost your family (beyond legal fees)

Time is the biggest hidden cost. In practice, delays can mean late mortgage payments, frozen business operating cash, or a long pause before a home can be sold. The New York State Unified Court System publishes practical information about Surrogate’s Court and probate basics at nycourts.gov.

A common scenario in Brooklyn is a two-asset estate: a co-op in Sheepshead Bay and a handful of bank accounts. Even with a will, the co-op board often requires executor authority, and the bank may want court papers before releasing funds. Avoiding probate in New York is really about controlling how assets are titled and transferred so your family is not waiting on court to move forward.

Key New York Probate Avoidance Strategies for Families

The best New York probate avoidance strategies combine simple tools with careful coordination. When plans fail, it is usually because someone picked one tactic (like adding a child to a deed) without thinking about taxes, creditor risk, or sibling dynamics.

Strategy 1: Use beneficiary designations where they fit

Retirement accounts and life insurance often transfer by beneficiary designation, not by will. Many bank and brokerage accounts can be set up as “payable on death” or “transfer on death,” depending on the institution. This is one of the cleanest ways to transfer cash quickly, as long as beneficiary forms are current and consistent with the overall plan.

Strategy 2: Joint ownership, but only with eyes open

Joint ownership can avoid probate, but it can also create problems. If you add an adult child to an account for convenience, you may be exposing that money to the child’s creditors or divorce. For divorcing parents in particular, “quick fixes” can complicate equitable distribution later. Avoiding probate court in New York should not increase your lawsuit or creditor exposure.

Strategy 3: A revocable living trust for real estate and “everything else”

For many families, a revocable living trust is the workhorse tool for how to avoid probate in New York. Properly drafted, it allows the successor trustee to manage and distribute trust assets without Surrogate’s Court. The key is not the document, it is implementation, which we will cover next. If you are comparing options, Living Trust v. Will, Which Protects Your Family Better? lays out practical differences.

Strategy 4: Consider long-term care planning alongside probate avoidance

Caregivers often ask, “If we avoid probate, does that protect the house from nursing home costs?” Not necessarily. Probate avoidance is about court process, while Medicaid planning is about eligibility rules and estate recovery. If long-term care is part of your reality, read Shielding Your Family's Inheritance from Medicaid Spend-Down: A Comprehensive Guide for Brooklyn Families.

The best plans align all of it, your probate avoidance strategy, your tax strategy, and your long-term care risk, so one decision does not undermine another.

Funding a Revocable Living Trust in NY: A Step-by-Step Guide

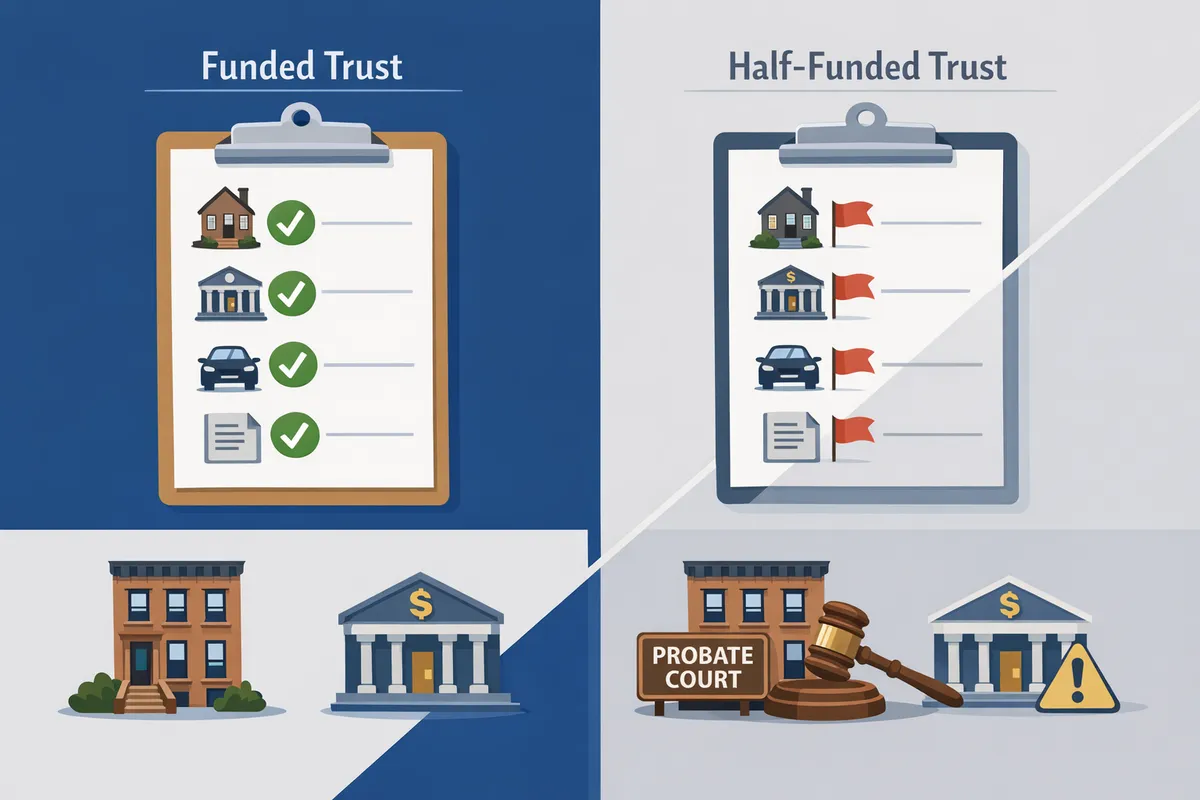

Funding a revocable living trust in NY is the difference between “paper planning” and a plan that actually avoids probate. I have seen beautifully drafted trusts that failed because the home stayed in the individual’s name, or because new accounts were opened years later and never titled correctly.

Here is the framework we use to keep families on track.

Step 1: List every asset and how it is titled right now

Start with the basics: your home (deed or co-op shares), bank accounts, brokerage accounts, life insurance, retirement accounts, and any business interests (LLC membership, shares, or partnership interests). Small business owners should also flag operating accounts and key contracts. You cannot fund what you have not identified.

Step 2: Transfer real estate, the right way for NY property

For a house, condo, or multi-family property, funding often means a new deed from you individually to you as trustee of your trust. Co-ops are different: many require assignment paperwork and board coordination. This is why “putting house in trust to avoid probate” is not a DIY weekend project. If you own real estate, A Homeowner's Guide to Putting Your Home in a Trust walks through common New York pitfalls.

Step 3: Retitle non-retirement accounts into the trust

Most checking, savings, and brokerage accounts can be retitled to the trustee of the trust. This is often where families get stuck because bank procedures vary. Bring your trust certification, government ID, and be prepared for a follow-up appointment.

A practical tip from our experience: if you are a caregiver and you need bill-pay continuity, retitle one primary household account first, confirm you can still pay everything, and then move secondary accounts.

Step 4: Coordinate beneficiaries, do not blindly move everything

Retirement accounts are usually not retitled to a revocable trust; they keep beneficiary designations for tax reasons. Life insurance stays in your name but can name the trust as beneficiary in certain situations (for example, minor children or special distribution needs). The goal is probate avoidance without creating an income tax surprise. For tax planning context, see How Do I Avoid Estate Taxes?.

Step 5: Create a “pour-over” will and keep the plan maintained

A pour-over will catches assets left outside the trust and “pours” them into it, but those assets may still require probate. That is why the last step is maintenance. When you open a new bank account, buy a new property, or form a new LLC, revisit funding. Why You Should Update Your Estate Plan is a useful reminder of when to review.

Common Challenges and How to Avoid Probate Court in New York

Most families do not fail at avoiding probate in New York because they lack documents, they fail because of mismatched details. The problems usually appear after death, when it is too late to “fix” title.

One frequent issue is the “half-funded trust.” For example, the Brooklyn brownstone is in the trust, but the largest savings account is still in the individual name. The family assumes the trust controls everything, then learns Surrogate’s Court is still required for that account.

Another challenge is using joint ownership as a shortcut. Adding an adult child to a deed can create unintended gifts and future creditor exposure. It can also cause sibling conflict, especially if one child is on title and others are not. If capital gains are a concern, remember that inheritance planning can preserve a step-up in basis; the IRS explains basis rules in Publication 551.

Finally, business owners often forget succession mechanics. If your LLC operating agreement does not clearly authorize a successor manager or transfer rules at death, your family may face delays even if you avoided probate elsewhere. This is where a coordinated estate plan and business plan really earns its keep.

Practical New York Estate Planning Tips to Secure Your Family’s Future

The best New York estate planning tips are the ones your family will actually follow under stress. In my nearly 30 years working with Brooklyn families, “simple and clear” beats “fancy and fragile” every time.

First, pick the right decision-makers. Your executor and trustee should be organized, calm, and comfortable with paperwork. For caregivers, this is often the adult child already coordinating doctors and bills. For small business owners, consider whether the same person should manage business operations or whether you need a separate business successor.

Second, build incapacity planning into probate avoidance. Probate happens at death, but financial chaos often starts earlier with illness or dementia. A durable power of attorney and a health care proxy let someone act while you are alive, so your trust plan is not your only safety net. If you want a deep dive, The Critical Role of a Healthcare Proxy in Your Estate Plan is a strong starting point.

Third, keep your “family meeting” mindset. A short, honest conversation about where documents are stored and who to call reduces conflict and prevents the last-minute scramble that pushes families into court.

Frequently Asked Questions About Avoiding Probate in New York

What are the disadvantages of avoiding probate?

The biggest disadvantage is that probate avoidance tools can create new risks if they are used without a full plan. Joint ownership can expose assets to a co-owner’s creditors or divorce, beneficiary designations can accidentally disinherit someone, and a trust that is not funded can give families a false sense of security. The solution is not to “avoid probate at all costs,” but to choose strategies that match your tax, long-term care, and family dynamics.

Which bank accounts avoid probate?

Accounts with a proper beneficiary or survivorship feature usually avoid probate. In practice, that can include joint accounts with right of survivorship and certain payable-on-death or transfer-on-death designations, depending on the bank’s policies. The key is documentation, the bank’s records control. If the designation is missing, outdated, or conflicts with your overall plan, the account may still require a court process to release funds.

Your Next Steps to Start Avoiding Probate in New York

Avoiding probate in New York is doable when you treat it like a system, not a single document. Start with clear goals, then match each asset to the right tool, beneficiary designations, trust funding, or coordinated ownership.

If you remember only one thing, make it this: a trust that is not funded is not a probate-avoidance plan. Update titles, confirm beneficiaries, and revisit the plan after major life changes.

If you want a structured, plain-English process that fits Brooklyn families, you can explore Secure Your Future: Expert Estate Planning Solutions Tailored to Your Needs. The right plan protects your people and your legacy, while keeping your family out of court when it matters most.