One legal document can protect your Brooklyn home from probate delays, but it can also create expensive surprises if it is drafted the wrong way. Life estate deeds are a common planning tool for New York homeowners who want to stay in their home for life and pass it to family later, often with Medicaid planning in mind.

If you are a caregiver trying to keep a parent safe in Bay Ridge, or a small business owner worried about liability, you are not alone in feeling confused. This guide explains how life estate deeds work, clears up myths, and shows where the strategy fits (and where it does not), especially for Medicaid recovery. For broader elder law context, start with What Medicaid Does (and Doesn’t) Cover in New York.

Ready to protect your home with a plan that fits your family? Schedule a Free Consultation to talk through your goals with Alatsas Law Firm.

Key Takeaways

- A life estate splits ownership into two layers: the life tenant keeps the right to live there, and the “remainderman” receives the property later.

- Life estate deeds in New York can avoid probate when the life tenant dies, but they do not solve every tax or Medicaid issue.

- Medicaid recovery is nuanced; life estate deed Medicaid recovery outcomes depend on timing and how the deed is structured.

- A life estate deed vs will comparison is not either-or; many Brooklyn families use both as part of a bigger plan.

- Tailoring matters most; small drafting choices can change control, creditor risk, and family harmony.

What Are Life Estate Deeds and How Do They Work in New York?

Life estate deeds let you give your home “later” while keeping the right to live in it “now.” In plain English, the deed splits the property into a present right and a future right. The person who keeps the right to live there is the “life tenant.” The person (or people) who automatically receive the home when the life tenant dies is the “remainderman.”

A common scenario we see in practice is a parent in Marine Park who wants to stay put, but also wants the home to pass to two adult children without probate. With a properly prepared deed, the transfer to the remaindermen happens automatically at death. That is one reason life estate deeds in New York are often discussed in estate planning meetings.

The control you keep, and the control you give up

The life tenant usually keeps possession, control of day-to-day living, and responsibility for expenses like property taxes and homeowner’s insurance. But the tradeoff is real: the life tenant generally cannot sell or refinance the home without the remaindermen agreeing, because they hold the future interest.

This is where family dynamics matter. If one child becomes estranged, or if a child is going through divorce or financial trouble, the “future interest” can become a pressure point.

Recording and practical follow-through

A life estate deed is only effective when it is properly executed and recorded. In New York City, recording typically runs through ACRIS, the NYC property records system. You can view the platform here: NYC ACRIS property records. Recording does not replace good planning, but it does create public notice and helps avoid title confusion later.

The big “next question” most families ask is whether they are giving away too much, or whether the deed is a Medicaid shortcut. That is where myths take over, so let’s address them directly.

Common Myths About Life Estate Deeds in New York Debunked

Most mistakes happen when families treat life estate deeds like a simple DIY probate hack. The deed can be powerful, but the assumptions people make about it are often wrong. Below are the biggest myths we hear from caregivers, young professionals, and small business owners across Brooklyn.

Myth 1: “I still own the house, so my kids can’t be affected.”

Reality: your remaindermen’s life events can affect your plan. If your child is sued, files bankruptcy, or is in the middle of divorce litigation, their future interest may become part of that problem. For a divorcing parent, this often connects with broader questions about asset division. If that is on your mind, it may be worth reading 401(k) and Divorce: Guide to Splitting Retirement Funds to see how courts and paperwork can reshape “separate” assets.

Myth 2: “A life estate deed overrides everything, so I don’t need a will.”

Reality: a deed only controls the house, not the rest of your estate. Your bank accounts, personal possessions, and who manages things if you become incapacitated are separate issues. Families often forget the emotional items that cause conflict. A helpful reminder is Memory Makers: Your Personal Possessions, because “stuff” can fracture families as quickly as real estate.

Myth 3: “This guarantees Medicaid protection.”

Reality: Medicaid planning is timing-sensitive and fact-specific. Life estate and Medicaid rules intersect, but a deed is not a magic shield. A rushed transfer during a crisis can trigger penalties and limit options.

Myth 4: “It’s always cheaper and simpler than a trust.”

Reality: the cheapest tool can be the most expensive mistake. For some families, a trust provides better control and fewer family consent issues. If you are wondering how to compare strategies, see When should a family consider a trust as part of an estate plan, and what type of trust should they use?.

If these myths sound familiar, the next step is comparing the deed to the tool most people already understand: a will.

Life Estate Deeds vs. Wills: Which Protects Your Family Better?

A life estate deed vs will comparison is really a question of what you are trying to protect: speed, control, privacy, or flexibility. A will is a set of instructions that generally requires probate to transfer a home. A life estate deed transfers the remainder automatically at death, often avoiding probate for that property.

If a homeowner in Bensonhurst puts the house in a will and leaves it equally to two children, the family may face probate timelines, court filings, and delays before they can sell or refinance. With life estate deeds, the house usually passes by operation of law when the life tenant dies.

Wills are still essential for “everything else.” Even when a life estate deed is used for the home, you still need a will (or a trust plan) to address personal property, guardianship issues, and to name the executor.

One overlooked difference is taxes. Families sometimes transfer the house to kids early and lose favorable tax treatment. The IRS explains “basis” and inherited property rules here: IRS Topic No. 703, Basis of Assets. The right structure can help preserve tax benefits while still meeting family goals.

So if wills and deeds each cover different risks, where does Medicaid fit, and why are Brooklyn families so concerned about “recovery”? Let’s get very specific.

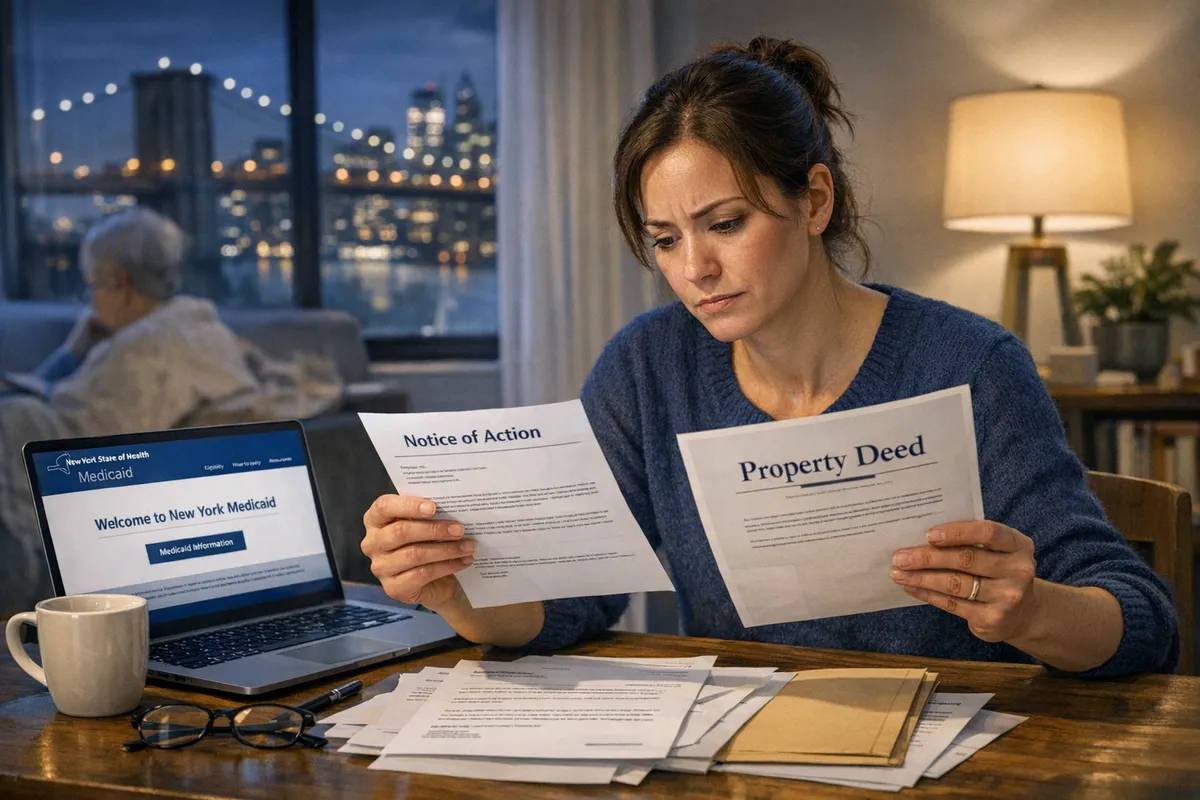

Medicaid Recovery and Life Estate Deeds: What Brooklyn Families Need to Know

The fear is real: families worry that a nursing home stay will force a home sale. In Brooklyn, we often see adult children caregiving while also juggling jobs, kids, and the emotional whiplash of a sudden hospitalization. If that is your season of life, the caregiver stress side of planning matters too, not just the legal paperwork. You may find 10 Strategies to Thriving as a Caregiver useful alongside the legal steps.

Medicaid eligibility versus Medicaid estate recovery

Medicaid eligibility rules and Medicaid estate recovery rules are related, but not identical. Eligibility focuses on whether the applicant qualifies for benefits. Estate recovery focuses on whether the state can seek reimbursement after death from assets in the recipient’s estate.

New York’s Medicaid program information is published by NYS Department of Health here: New York State Department of Health Medicaid. For official publications and guidance updates, see: NYSDOH Medicaid publications.

Where life estate deed Medicaid recovery questions get tricky

A life estate can change what is “in the estate” at death, but it does not erase every risk. A common Brooklyn life estate deed example looks like this: Mom owns a row house in Sunset Park, she signs a deed giving herself a life estate and naming her daughter as remainderman. Mom later receives Medicaid benefits.

At Mom’s death, the daughter becomes owner automatically. Whether Medicaid estate recovery can pursue a claim can depend on multiple factors, including how the state defines the estate for recovery purposes, the timing of transfers, and whether the home was otherwise protected by exemptions while Mom was alive.

Timing is often the make-or-break issue. If a deed is done during a crisis without considering Medicaid transfer rules, the family may trigger a penalty period that delays coverage. When that happens, families scramble to pay bills, sometimes by draining savings or taking on debt. In urgent situations, retroactive coverage can be part of the solution, and you can learn more here: Using Retroactive Medicaid Benefits to Prevent Financial Disaster.

The practical planning question to ask

Instead of asking, “Can a nursing home take a life estate?” ask this: What outcome do we need, and what is our timeline? If the goal is long-term asset protection, a Medicaid Asset Protection Trust may be a better fit than a deed in some cases. If the goal is simply avoiding probate while retaining occupancy, a life estate might be appropriate.

This is the point where a tailored plan matters more than any single document. Next, we will look at how to customize life estate deeds so they actually match Brooklyn families’ real risks.

Tailoring Life Estate Deeds for Effective Asset Protection in Brooklyn

A well-drafted life estate deed is not “one size fits all,” especially in Brooklyn where families often blend multigenerational living, small business ownership, and complex finances. The right design depends on what you are protecting against: probate delays, Medicaid recovery concerns, creditor exposure, or family conflict.

Brooklyn-specific scenarios that change the drafting

Small business owners often need extra creditor planning. If you run a contracting business in Gravesend and you put your child (who is also a co-owner of the business) on the deed as remainderman, you may be tying your home plan to business liability risk. For some families, keeping the home plan separate from business exposure is a key goal.

Blended families require extra clarity. If you are remarried and want your spouse to live in the home, but you want the property to go to children from a prior relationship, a life estate deed can sometimes support that intent. The drafting must be careful, and it must align with beneficiary designations and other estate documents.

A simple checklist before you sign anything

Before you commit to life estate deeds, confirm the “people risks,” not just the legal theory. In our experience, these questions prevent the most heartbreak:

- Can the remaindermen cooperate later? If siblings cannot agree, future sale or refinancing can become impossible.

- Are any remaindermen facing divorce, lawsuits, or debt? Future interests are not invisible to creditors.

- Do you need flexibility to move? Many homeowners later want to downsize or relocate closer to caregiving.

If your core goal is Medicaid-focused asset protection, you may also want to compare a deed to a trust structure. A helpful starting point is Should I put my primary residence in an irrevocable trust?.

Want a plan that protects your home and your family relationships? Start your journey with a guided intake and planning process: Start Your Journey.

The goal is not to “use a life estate deed.” The goal is to protect a home, reduce risk, and keep options open for care. Let’s answer the three questions people ask most online.

Frequently Asked Questions About Life Estate Deeds in New York

How much does it cost to do a life estate deed?

The cost depends on complexity, not just the paper. In Brooklyn, legal fees vary based on whether you need Medicaid planning analysis, multiple remaindermen, blended-family provisions, title issues, or coordinated updates to wills and powers of attorney. You may also have recording fees and possible transfer tax considerations depending on the facts. The cheapest quote can be costly if it ignores Medicaid timing or family consent problems.

Who owns the property in a life estate deed?

Both parties have ownership interests, but in different ways. The life tenant owns the present right to possess and use the home for life, while the remainderman owns the future interest that becomes full ownership at the life tenant’s death. In everyday terms, the life tenant usually controls living in the home, but major decisions like selling typically require everyone’s agreement.

Can you sell a property that has a life estate?

Yes, but typically only if the life tenant and all remaindermen agree. Because the remaindermen hold a future interest, a buyer usually wants a deed signed by everyone to deliver clear title. In real Brooklyn transactions, the problem is not legality, it is logistics: one remainderman who refuses to sign can stop a sale, even when the life tenant needs the money for care or a move.

Your Next Steps for Protecting a Brooklyn Home

Life estate deeds can be an elegant solution when they match your timeline, your family dynamics, and your long-term care plan. They are also easy to misunderstand, especially when internet advice blurs Medicaid eligibility with Medicaid recovery.

If you are trying to protect a parent’s home, or you are a business owner separating family wealth from business risk, focus on the tailoring. The right document is the one that preserves control today while protecting your family tomorrow.

When you are ready, talk through your options with a local attorney who understands Brooklyn neighborhoods and New York rules. Life estate deeds work best as part of a complete plan, not as a stand-alone shortcut.