Most American families want to protect their homes for the next generation, but misunderstandings about life estates create real risks. Nearly half of property owners believe a life estate works the same way as traditional ownership, when in fact, it comes with unique limits and legal twists. By clarifying what a life estate really means and exposing common myths, you gain the insight needed to make confident decisions about your family’s legacy.

Key Takeaways

| Point | Details |

|---|---|

| Understanding Life Estates | A life estate allows property ownership for a person’s lifetime, with restrictions on transfer and modifications by the life tenant. |

| Consultation is Crucial | Families should seek legal advice from an estate planning attorney to navigate the complexities of life estates and ensure protection of their interests. |

| Tax and Medicaid Implications | Life estates can impact tax liabilities and Medicaid eligibility, necessitating careful financial planning to avoid unexpected consequences. |

| Define Responsibilities Clearly | Establishing explicit agreements between life tenants and remaindermen helps to prevent conflicts regarding property maintenance and financial obligations. |

Defining Life Estates and Common Misconceptions

A life estate represents a unique legal arrangement that allows property ownership with specific time-limited conditions. According to Cornell Law School’s legal definitions, a life estate is an interest in property that exists only for the duration of a specific person’s lifetime. Unlike traditional property ownership, the holder cannot transfer the property through a standard will, as their interest automatically terminates upon their death.

The core mechanism of a life estate involves creating a property arrangement where the original owner (known as the life tenant) retains full rights to use and occupy the property during their lifetime. As Forbes explains, this approach enables property transfer to heirs while guaranteeing the original owner can remain in their home throughout their remaining years. This strategy provides flexibility for families seeking to manage property inheritance while maintaining the current occupant’s residential stability.

Common misconceptions about life estates often revolve around property rights and transferability. Many Brooklyn families mistakenly believe that a life estate functions exactly like traditional property ownership. However, critical differences exist: the life tenant cannot sell the entire property outright, cannot make permanent structural modifications without potential legal complications, and cannot will the property to someone else after their death. The remainder interest holders (typically children or designated beneficiaries) will automatically receive full property rights once the life tenant passes away.

Pro Tip for Brooklyn Families: Carefully consult with an estate planning attorney before establishing a life estate, as the legal nuances can significantly impact your family’s long-term property management and inheritance strategies.

Types of Life Estates and How They Differ

Life estates come in multiple variations, each with unique legal characteristics that impact property ownership and inheritance strategies. According to legal definitions, a fundamental structure involves creating a deed that specifies property ownership for a specific duration, typically tied to an individual’s lifetime. For instance, a deed might state “to John Doe for life, then to Jane Doe,” which establishes John as the life tenant and Jane as the remainder interest holder.

Two primary categories of life estates exist: conventional and legal life estates. Conventional life estates are intentionally created by property owners through specific legal documents like deeds or wills. These arrangements explicitly outline how property will be managed during the life tenant’s lifetime and what happens upon their death. Legal life estates, conversely, are automatically established by law, such as spousal inheritance rights that provide a surviving spouse with property interests without requiring explicit prior documentation.

The mechanics of life estates involve complex property transfer rules that differ significantly from traditional ownership. A life tenant can use and potentially generate income from the property, but cannot make permanent alterations that might diminish the property’s long-term value. For Brooklyn families considering this strategy, understanding these nuanced restrictions is crucial. The remainder interest holders maintain future ownership rights, which means any substantial changes to the property must consider both current and future owners’ potential interests.

Pro Tip for Property Planning: Always consult with an experienced estate planning attorney to understand the specific implications of different life estate structures for your unique family situation and local legal requirements.

How Life Estates Work in Brooklyn Property Law

Brooklyn property law recognizes life estates as a nuanced legal mechanism that provides unique ownership protections for families navigating complex inheritance scenarios. Understanding the potential challenges with life estates requires a deep examination of local legal frameworks that govern property transfers and inheritance rights. In New York, life estates offer a strategic approach for property owners seeking to maintain residential stability while preparing for future generational transitions.

The mechanics of life estates in Brooklyn involve intricate legal arrangements that balance current occupancy rights with future inheritance expectations. A life tenant retains full residential rights, including the ability to live in the property, generate rental income, and cover maintenance expenses. However, critical limitations exist: the life tenant cannot sell the entire property, make permanent structural modifications without potential legal complications, or transfer complete ownership through a standard will. These restrictions protect the remainder interest holders’ future property rights, ensuring the asset remains within the family’s intended inheritance plan.

New York’s specific property laws add additional complexity to life estate arrangements. Brooklyn families must navigate state-specific regulations that impact property transfers, tax implications, and potential Medicaid considerations. Factors such as local zoning laws, property tax assessments, and inheritance statutes can significantly influence how a life estate functions. Blended families, in particular, face unique challenges when establishing life estates, as estate planning requires careful navigation of familial relationships and legal boundaries.

Pro Tip for Brooklyn Property Owners: Consult a local estate planning attorney who understands the intricate nuances of New York property law to ensure your life estate strategy provides maximum protection and flexibility for your family’s specific circumstances.

Rights and Responsibilities of Life Tenants and Remaindermen

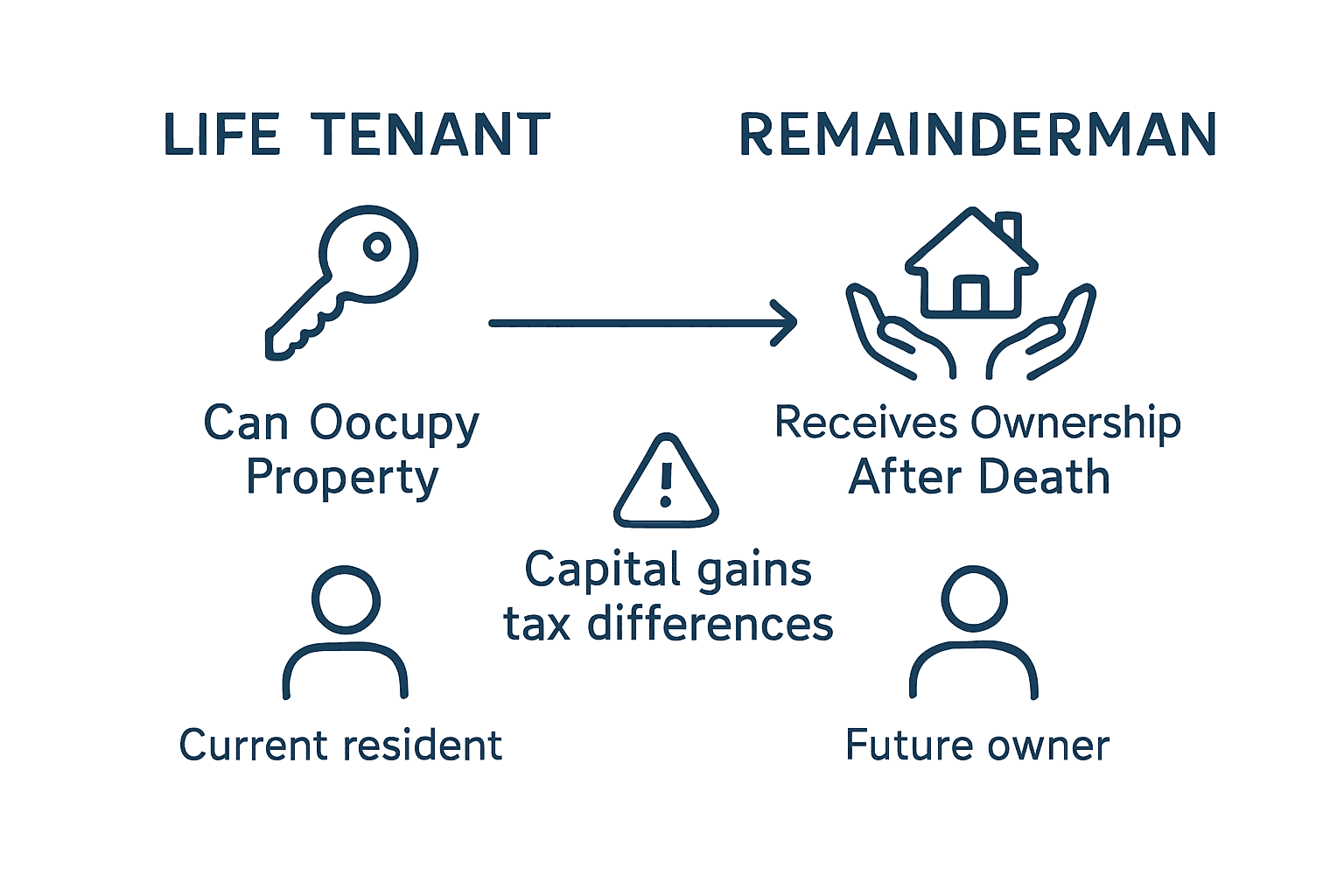

Life tenants and remaindermen have distinctly defined roles that create a delicate balance of property rights and responsibilities. According to legal definitions, the life tenant possesses full rights to use and occupy the property during their lifetime, with the critical limitation that they cannot permanently transfer the property through a standard will. This unique arrangement means the life tenant can live in, rent, or generate income from the property, but must also preserve its fundamental value for future inheritors.

The responsibilities of life tenants extend beyond simple occupancy. They are legally obligated to maintain the property, pay property taxes, and ensure the asset remains in good condition. Critically, life tenants cannot commit waste - actions that would substantially decrease the property’s value or structural integrity. Remaindermen, who hold a future interest in the property, have the legal right to protect their inheritance by monitoring the life tenant’s maintenance and preventing any actions that might compromise the property’s long-term worth.

Financial and legal complexities further define the relationship between life tenants and remaindermen. Life tenants can transfer their interest during their lifetime, but this transfer does not alter the fundamental structure of the life estate. Remaindermen maintain a vested future interest, which means they are legally positioned to inherit the full property ownership once the life tenant passes away. This intricate arrangement requires careful documentation and often benefits from professional legal guidance to ensure all parties’ rights are fully protected and understood.

Here’s a concise comparison of life tenant and remainderman roles in a life estate:

| Role | Main Rights | Key Responsibilities | Limitations |

|---|---|---|---|

| Life Tenant | Occupy and use property | Maintain property and pay taxes | Cannot sell or will full property |

| Remainderman | Guaranteed future ownership | Protect long-term property value | No occupancy until life tenant passes |

Pro Tip for Property Owners: Develop a clear, written agreement between life tenants and remaindermen that explicitly outlines maintenance expectations, financial responsibilities, and potential dispute resolution mechanisms to prevent future conflicts.

Tax, Medicaid, and Asset Protection Considerations

Life estates present complex financial implications that extend far beyond simple property ownership. Comprehensive Medicaid asset protection strategies become critical when understanding how these arrangements interact with government benefits, tax obligations, and long-term financial planning. Brooklyn families must carefully navigate the intricate landscape of potential tax consequences, Medicaid eligibility, and asset preservation strategies inherent in life estate structures.

The tax ramifications of life estates can be particularly nuanced. Remaindermen may face unexpected capital gains tax scenarios, as the property’s cost basis is determined by the original purchase price rather than its value at the time of inheritance. This means potential significant tax liabilities when the property is eventually sold. Medicaid planning adds another layer of complexity, as the life estate can impact eligibility for long-term care benefits. Strategic approaches to avoiding Medicaid penalties require careful timing and precise legal structuring to protect both residential stability and potential government assistance.

Asset protection emerges as a critical consideration for families establishing life estates. The structure provides a unique mechanism for preserving property within a family while offering some shield against potential creditors. However, this protection is not absolute. Different scenarios can compromise the asset protection benefits, including improper maintenance, unexpected legal challenges, or failure to comply with specific legal requirements. Brooklyn families must work closely with experienced estate planning professionals to ensure their life estate strategy provides maximum financial security and meets their specific long-term care and inheritance objectives.

Below is a summary of how life estates influence financial planning for Brooklyn families:

| Consideration | Life Estate Impact | Planning Implication |

|---|---|---|

| Taxes | May trigger capital gains for heirs | Review basis and timing with expert |

| Medicaid | Affects eligibility calculations | Proper structuring avoids penalties |

| Asset Protection | Shields property, but not absolute | Maintain compliance for best results |

Pro Tip for Financial Planning: Conduct a comprehensive review of your life estate strategy with a qualified estate planning attorney who understands the intricate interactions between property ownership, tax implications, and Medicaid regulations specific to New York State.

Avoiding Mistakes When Creating a Life Estate

Creating a life estate requires meticulous legal and financial planning to prevent costly errors that could compromise your family’s long-term property interests. Understanding estate planning pitfalls becomes critical when structuring these complex property arrangements. Brooklyn families must recognize that seemingly minor oversights can result in significant legal and financial consequences that potentially undermine their original inheritance intentions.

Common mistakes in establishing life estates often stem from misunderstanding critical legal nuances. Families frequently fail to fully comprehend the tax implications for remaindermen, who may unexpectedly inherit substantial capital gains tax obligations. Another frequent error involves inadequate consideration of Medicaid eligibility, where improper life estate structuring can inadvertently disqualify the life tenant from crucial long-term care benefits. Proper documentation, precise language in property transfer documents, and thorough understanding of New York State’s specific legal requirements are essential to avoiding these potential pitfalls.

The relationship between life tenants and remaindermen requires careful, proactive management to prevent future conflicts. Families must establish clear expectations about property maintenance, potential improvements, and financial responsibilities. Unexpected scenarios such as necessary property repairs, tax assessments, or changes in family dynamics can create tension if not explicitly addressed in the initial life estate agreement. Professional legal guidance becomes invaluable in anticipating and mitigating these potential sources of disagreement, ensuring the life estate serves its intended purpose of preserving family property and maintaining generational harmony.

Pro Tip for Legal Precision: Work exclusively with an estate planning attorney specialized in New York property law to draft your life estate documents, ensuring every detail is carefully considered and legally sound.

Secure Your Family’s Future with Expert Life Estate Guidance

Understanding the complexities of a life estate can be overwhelming for Brooklyn families facing important decisions about property ownership, inheritance, and Medicaid planning. This legal tool offers unique benefits but also carries specific responsibilities and risks, such as managing tax consequences, protecting assets, and ensuring your intentions are honored across generations. If you want to avoid common mistakes and properly balance the rights of life tenants and remaindermen, expert legal advice is essential.

At Alatsas Law Firm, we specialize in helping Brooklyn families navigate these challenges through personalized estate planning and elder law strategies. Gain peace of mind knowing your life estate is structured correctly and aligned with your financial and family goals. Learn more about our approach to Medicaid asset protection and estate planning for blended families. Take control of your property’s future today and avoid costly errors by scheduling a consultation with our experienced team at Schedule Your Consultation. Your family’s security deserves attention now.

Frequently Asked Questions

What is a life estate?

A life estate is a legal arrangement that allows an individual (the life tenant) to use and occupy a property for the duration of their lifetime, after which ownership passes to predetermined heirs (remaindermen).

How do life estates differ from traditional property ownership?

Unlike traditional ownership, a life tenant cannot sell or will the property. Their rights are limited to use and occupancy during their lifetime, and they cannot make permanent modifications that affect the property’s value without consent from the remaindermen.

What are the responsibilities of a life tenant?

The life tenant is responsible for maintaining the property, paying property taxes, and ensuring it remains in good condition. They must avoid actions that would significantly diminish the property’s value, a concept known as avoiding waste.

What should families consider before establishing a life estate?

Families should consult with an estate planning attorney to understand potential tax implications, Medicaid eligibility, and the specific legal nuances of life estates to ensure they align with their long-term property management and inheritance goals.