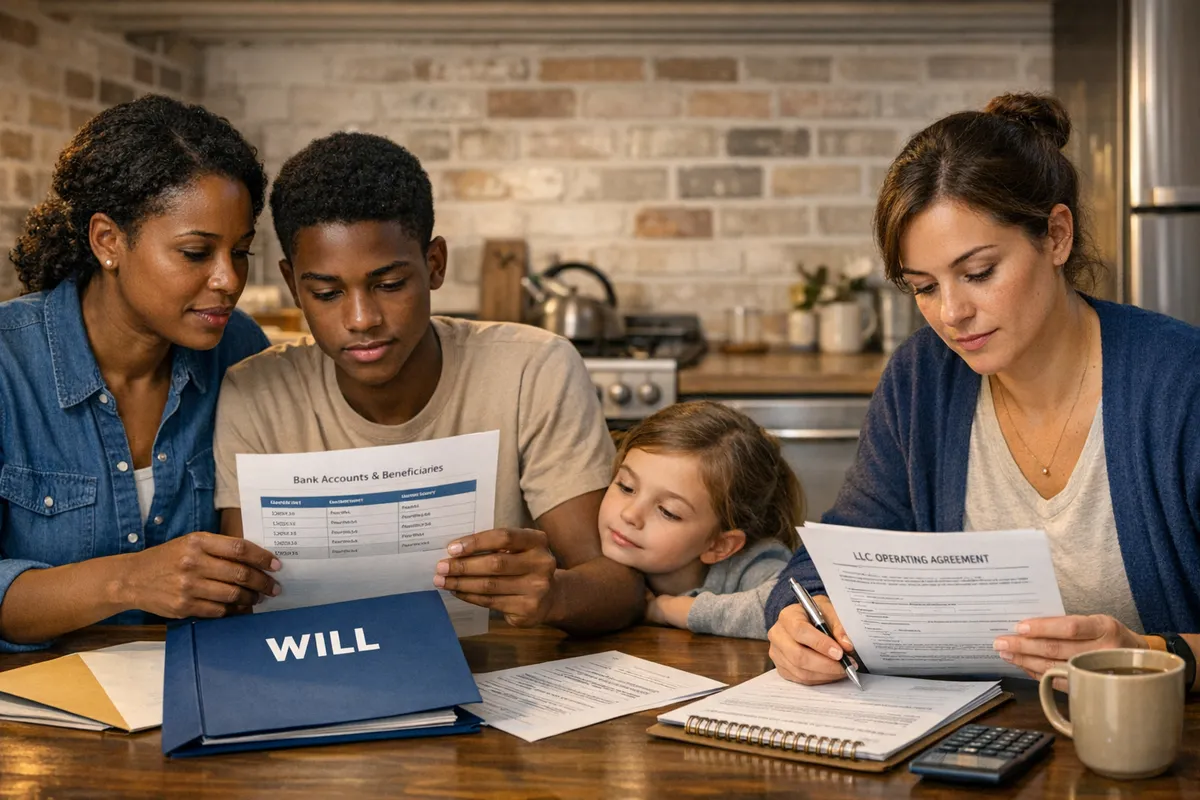

If you have ever wondered, "what are some common mistakes in estate planning people make," you are already ahead of the families who learn the hard way. In our Brooklyn practice, we routinely meet small business owners, caregivers, and young professionals who assumed estate planning was “for the wealthy” until a crisis forced the issue.

A solid plan is not about fancy documents, it is about risk reduction. Below, we will walk through the most common estate planning mistakes to avoid, how they create probate and family conflict in New York, and how to fix them with a will or properly funded trust that actually works. For a trust overview, start here: When should a family consider a trust as part of an estate plan, and what type of trust should they use?

Ready to start protecting your family (without guesswork)? Schedule a Free Consultation and get a clear, plain-English plan.

Key Takeaways

- A plan that is not funded is not a plan; the importance of funding your trust properly is what turns paperwork into real protection.

- Probate delays are usually preventable when beneficiaries, assets, and executor authority are set up correctly.

- “We are middle-class, we do not need this” is a myth; what are some common mistakes in estate planning people make often starts with waiting.

- Life changes break old documents; divorce, a new baby, or a new business entity should trigger an update.

- A simple risk-reduction framework works: identify risks, protect the people, plan the instructions, then fund the plan.

Understanding What Are Some Common Mistakes in Estate Planning People Make

The biggest risk is assuming your family will “figure it out.” When people ask, “what are some common mistakes in estate planning people make,” they are usually picturing extreme situations, like celebrities fighting over estates. In real middle-income households, the mistakes are smaller and more common, and that is exactly why they are dangerous.

A common scenario is a Bay Ridge couple with a paid-off co-op, some retirement savings, and one adult child. They think, “Everything goes to our child anyway.” Then one spouse dies, the survivor is overwhelmed, and the child finds out a bank account has no payable-on-death designation, the co-op’s transfer rules are strict, and nobody can locate the original will.

The “identify, protect, plan, fund” lens

To reduce risk, we like a simple framework:

- Identify what you own and what could go wrong (incapacity, lawsuits, long-term care, second marriages).

- Protect decision-makers (powers of attorney, health care proxy) and vulnerable beneficiaries.

- Plan how assets transfer (will, trust, beneficiary designations).

- Fund the plan by aligning titles and beneficiaries with your documents.

In our experience, the most common estate planning mistakes to avoid in New York include: no incapacity planning, relying on handwritten notes, and forgetting that accounts with beneficiaries transfer outside the will. If you are not sure what happens without a will, read: What Happens When You Die Without a Will?

The good news is that once you see the pattern, you can fix it. Next, let’s talk about the estate planning errors that cause probate delays and how to prevent them.

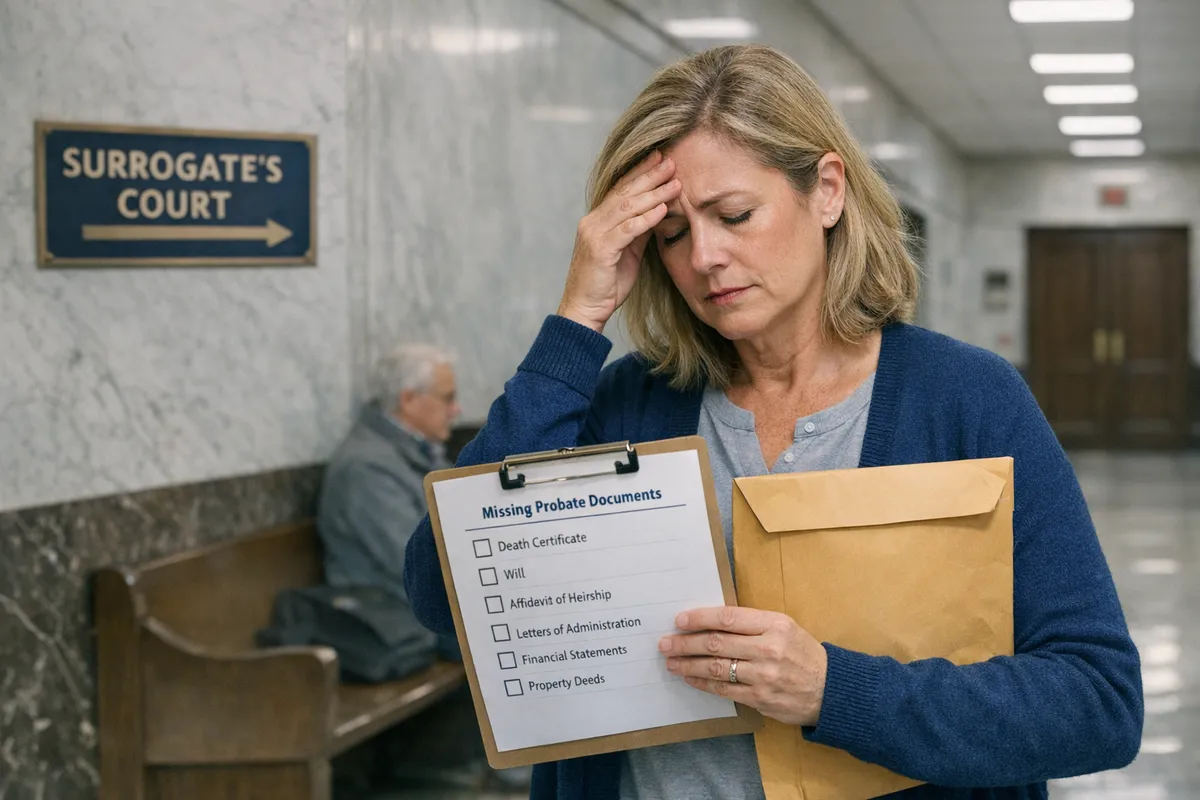

Critical Estate Planning Mistakes That Cause Probate Delays and How to Avoid Them

Probate is not automatically “bad,” but unnecessary probate delays are brutal on grieving families. In Kings County Surrogate’s Court, delays usually come from missing information, missing signatures, family disputes, or assets that were never organized. These are classic estate planning errors that cause probate delays.

One anonymized example from near Sheepshead Bay: an adult daughter tried to probate her father’s will, only to discover the named executor had moved out of state and would not cooperate. The will did not name a backup executor, and the family did not have a clean list of accounts. Months passed while the court process crawled forward, and the family kept paying carrying costs on an apartment.

Mistake 1: Using the wrong people (or no backups)

Executor and trustee choices are not honorary titles. If the person is unavailable, unwilling, or overwhelmed, your estate can stall. Naming backups and confirming they can serve is one of the simplest fixes.

Mistake 2: Outdated beneficiaries and missing asset details

A will does not control everything. Retirement accounts, life insurance, and many transfer-on-death designations bypass probate. A divorce or death can leave outdated beneficiaries in place, which creates conflict and confusion. To keep your information current, see: Is Your Financial Information Up to Date?

For New York probate basics straight from the source, the NY Courts overview is helpful: New York State Unified Court System, Surrogate’s Court

Mistake 3: “DIY” documents that fail under pressure

Online forms can be tempting for cost reasons, especially for young professionals. But in practice, they often fail on execution formalities, unclear language, or missing companion documents. A will without a power of attorney still leaves your family stuck if you are alive but incapacitated.

Avoiding these delays is not only about having documents. It is also about making sure your trust, if you have one, actually owns what it is supposed to own.

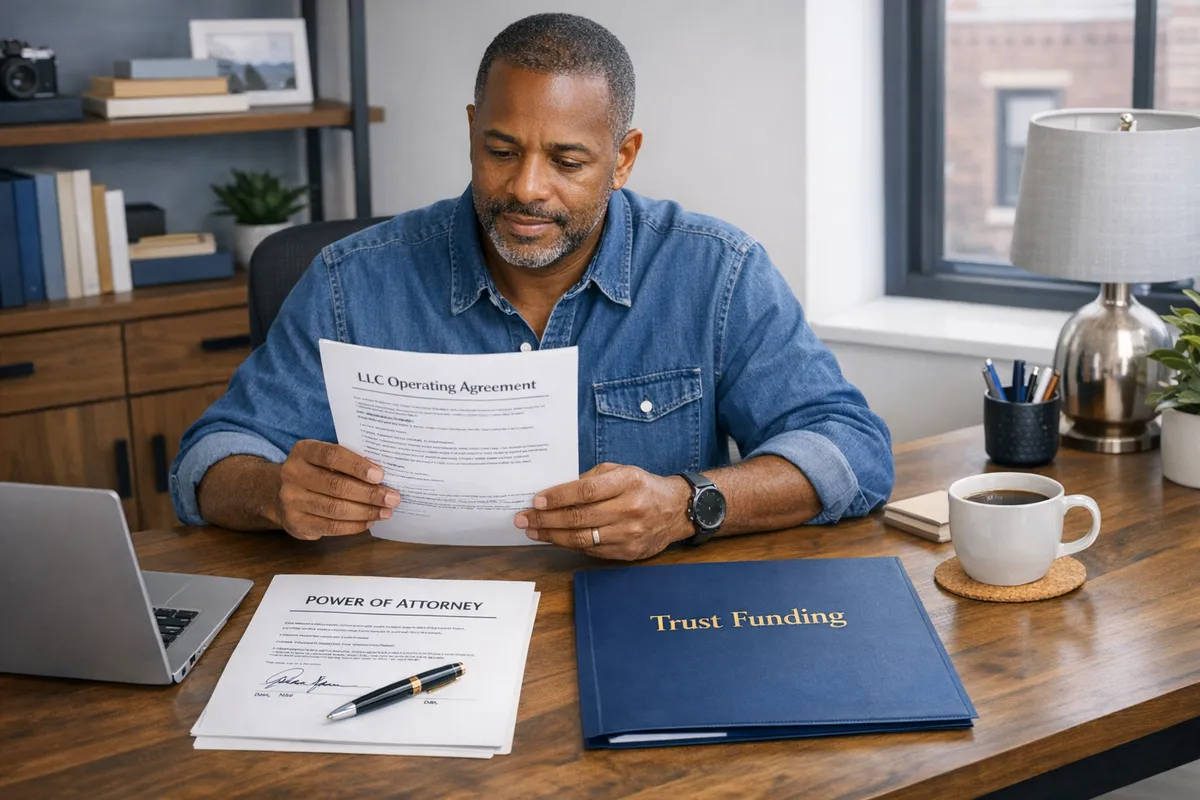

The Importance of Funding Your Trust Properly: Protecting Your Family’s Legacy

A trust that is not funded is like a safe that never got bolted to the floor. Clients often do the hard part, they sign a revocable living trust, then they stop. That is why the importance of funding your trust properly cannot be overstated.

Funding means re-titling assets so the trust, not you individually, owns them (or coordinating beneficiary designations where appropriate). In a typical middle-class New York estate, the key funding targets are the home (or co-op shares, if allowed), non-retirement bank accounts, and sometimes a brokerage account.

A real-world Brooklyn example: a small business owner created a trust to keep things private and efficient for his spouse, but his primary checking account and a savings account remained in his individual name. When he died, those accounts still required a probate filing, even though the trust existed. One missed step created months of delay and added legal fees.

Trust funding mistakes we see most

The common estate planning mistakes to avoid here are surprisingly consistent:

- Forgetting to transfer the home, or transferring it incorrectly.

- Funding some accounts but not the “everyday” accounts.

- Ignoring business interests, like LLC membership interests.

If your home is part of the plan, this primer answers a frequent question: Should I put my primary residence in an irrevocable trust?

For tax reality-checks, the IRS explains basis rules and related topics here: IRS, Basis of Assets

The next step is making sure the overall plan is designed for the realities of middle-class families, including caregiving, divorce, and small business risk.

How to Fix Estate Planning Mistakes and Build a Solid Plan for Middle-Class Families

Fixing problems is usually less dramatic than people fear, it is a guided cleanup. When someone asks how to fix estate planning mistakes, we start by mapping the risks that matter most to their life, not the risks that look impressive on paper.

Consider three common Brooklyn households:

- A caregiver managing a parent’s early dementia.

- A divorcing parent trying to keep beneficiary designations aligned with a new custody and support reality.

- A small business owner with an LLC and personal assets that could be exposed if the business is sued.

A practical “repair checklist” that works

Here is the order that tends to reduce risk fastest:

- Update your decision-makers (agent under power of attorney, health care proxy, HIPAA access).

- Confirm your distribution plan (who gets what, and when, especially for minors or vulnerable adults).

- Coordinate titles and beneficiaries to match the plan.

- Add the right protection tools for your scenario, such as trusts or business succession provisions.

This is also where family dynamics matter. If you have personal property with emotional value, do not leave it to guesswork. A simple written personal property memorandum can prevent fights over jewelry, heirlooms, and collections. For ideas, read: Memory Makers: Your Personal Possessions

The most effective fixes are the ones your family can execute quickly. That means clear instructions, the right agents, and documents stored where your people can access them. Next, let’s get specific with middle-class estate planning tips you can act on this week.

Middle-Class Estate Planning Tips: Practical Steps to Safeguard Your Family’s Future

You do not need a million-dollar net worth to need a plan, you need people who depend on you. Middle-class estate planning tips are most useful when they translate into calendar actions, not vague intentions. If you are still asking what are some common mistakes in estate planning people make, this section is your “do it now” playbook.

Tip 1: Treat beneficiary designations like part of your estate plan

Beneficiary designations can override your will. Check them after marriage, divorce, a new child, or a death in the family. A 20-minute review can prevent a multi-year lawsuit.

Tip 2: Build in long-term care reality

Caregiving families often fear losing everything to nursing home costs, and that fear is not irrational. Planning options exist, but timing and strategy matter. If you want a plain-English overview of what counsel can do, see: What Can an Elder Law Attorney do For You?

Tip 3: Align your business and personal plan

For entrepreneurs, your estate plan should reference succession and authority. If you are incapacitated, who can sign for the business? Who can access the operating agreement? Business continuity is family protection when the household depends on that income.

Tip 4: Do not ignore “no heirs” or nontraditional family structures

Not every plan is spouse-and-kids. If you are single, child-free, or your closest relationships are friends or extended family, New York’s default rules may not match your wishes. This is where a custom plan is essential: Estate Planning With No Heirs

Want a step-by-step process that ends with a funded plan? Start here: Start Your Journey.

With these practical steps in place, the remaining work is answering the questions families ask most often when they are trying to avoid the common estate planning mistakes to avoid.

Frequently Asked Questions About Common Estate Planning Mistakes

Do I need a trust, or is a will enough in New York?

It depends on your goals, but many families start with a will and add a trust for probate avoidance and privacy. A will is essential for naming guardians for minor children and directing assets that do not have beneficiaries. A trust can reduce probate involvement for assets titled to the trust. The key is matching the tool to the problem, then funding it.

What is the fastest way to avoid probate delays for my family?

The fastest way is to organize assets and align titles and beneficiaries with your plan. Probate delays often come from missing account information, outdated beneficiary designations, and disputes over who has authority to act. Naming backups for executors and keeping a current asset list for your family can save months, especially in New York.

Can I fix estate planning mistakes after a divorce?

Yes, but you should act quickly because old documents can conflict with new legal and family realities. After divorce, you may need to update your will, power of attorney, health care proxy, and beneficiary designations, and you may need trust provisions that reflect custody and support obligations. An attorney can also help you avoid accidental disinheritance or unintended benefits to an ex-spouse.

Your Next Steps to Protect Your Family’s Future

Even small oversights can derail an otherwise solid plan, but they are fixable. The families who avoid stress later are the ones who treat estate planning as a risk-reduction project, not a one-time purchase.

If you take only one action after reading about what are some common mistakes in estate planning people make, make it this: get a basic will or trust in place, then make sure it is properly funded and updated. If you are in Brooklyn or surrounding neighborhoods, Alatsas Law Firm can help you identify risks, protect your decision-makers, plan your transfers, and fund the plan so it works when your family needs it most.