When a Brooklyn brownstone is your family’s biggest asset, the fear is real: one nursing home stay could wipe out a lifetime of work. For many caregivers and small business owners, Protecting Home Equity in Brooklyn’s High-Value Neighborhoods for Medicaid Eligibility feels confusing, or like it is “only for rich families.” It is not.

This guide walks you through how Medicaid looks at home equity in New York, what actually puts eligibility at risk, and how a Brooklyn family typically moves from first questions to a signed, funded plan. For background on coverage, start with What Medicaid Does (and Doesn’t) Cover in New York.

Ready to get clarity fast? Start your journey with Alatsas Law Firm’s intake form: Start Your Journey

Key Takeaways

- Your primary residence can be exempt for Medicaid eligibility, but home equity limits can still matter depending on circumstances.

- Timing is the whole game because New York’s lookback rules can penalize certain transfers if you wait too long.

- Protecting Home Equity in Brooklyn’s High-Value Neighborhoods for Medicaid Eligibility often involves trusts, smart spending, and careful documentation, not “hiding money.”

- DIY transfers can backfire by triggering taxes, creditor risk, or Medicaid penalties.

- A step-by-step plan reduces stress for caregivers managing family dynamics and urgent care decisions.

Understanding Medicaid Eligibility and Home Equity Limits in Brooklyn

Medicaid eligibility is not just about income, it is about how your assets are titled and counted. In Brooklyn, this gets intense because a modest row house in Bay Ridge or a co-op near Prospect Park can be worth far more than people expect.

Here is the core concept: your primary residence is often treated differently than cash. For many applicants, a home can be an “exempt” resource while they are alive, especially if they intend to return home. But New York also has home equity limits for certain Medicaid long-term care situations. If your equity exceeds the limit, it can block eligibility even when the home is your primary residence. (These limits change over time, so you always confirm current numbers before filing.)

A common Brooklyn scenario is a middle-income family caregiver in Ditmas Park. Mom needs nursing home level care, and the only “asset” is the house. The adult child is worried Medicaid will “take the house immediately.” In practice, Medicaid is more complicated: eligibility rules, estate recovery rules, and transfer rules all intersect.

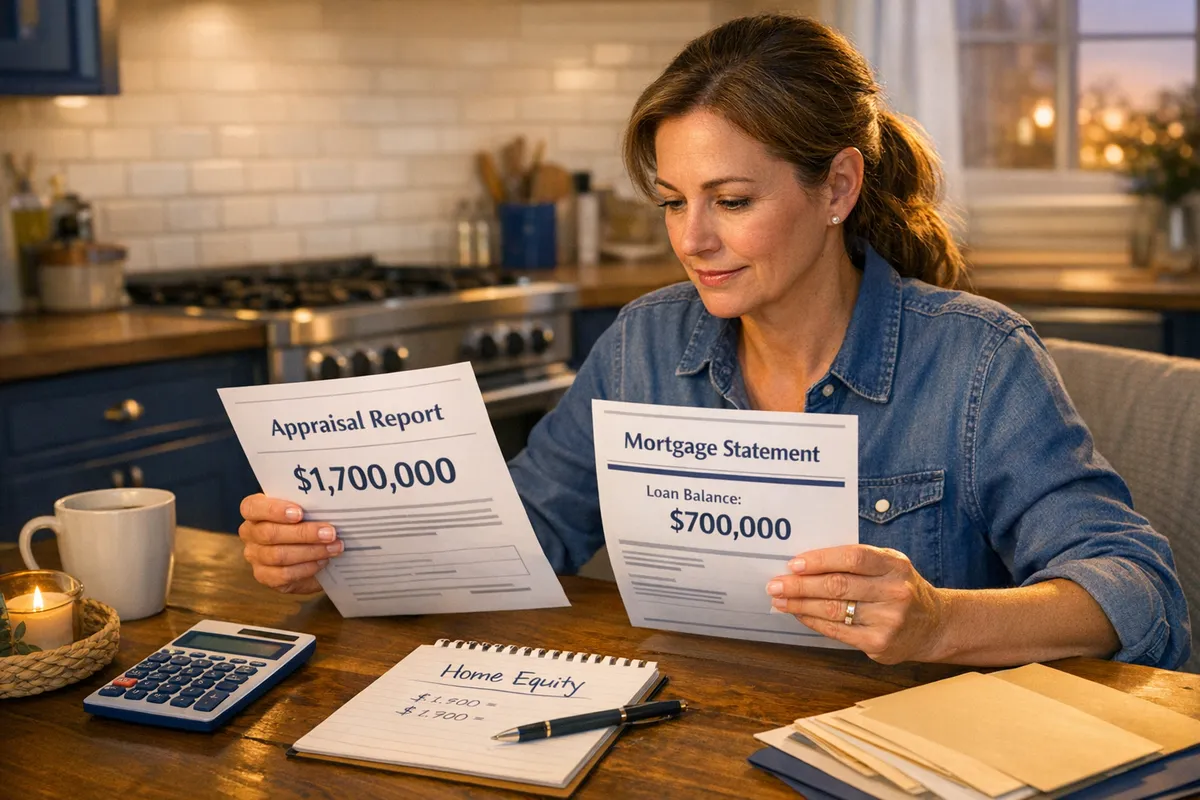

What “home equity” means in plain English

Home equity is the value of the home minus valid mortgages and liens. If you have a $1.7M home in Brooklyn Heights and a $700K mortgage, your equity is not $1.7M, it is about $1.0M. Even that number can matter for Brooklyn high-value home Medicaid rules.

For official context on New York Medicaid generally, review the New York State Department of Health Medicaid page: NYSDOH Medicaid.

To move from confusion to control, you first need to clear up the biggest myths that cause families to wait until it is too late.

Common Misconceptions About Medicaid Planning for Brooklyn Homeowners

The biggest mistake we see is waiting because you think you “do not have enough money” to plan. Medicaid planning for Brooklyn homeowners is often most valuable for families who have a home and not much else.

Misconception #1: “Medicaid planning is only for wealthy families.” Reality: a single Brooklyn home can create eligibility problems even for middle-income households, especially when long-term care is involved.

Misconception #2: “If I put the house in my child’s name, we are protected.” Reality: simple deeds can trigger Medicaid penalties and create new risks, like divorce claims, lawsuits, creditor liens, and capital gains tax surprises.

Misconception #3: “Medicaid will seize the home the day my parent goes into a nursing home.” Reality: Medicaid is primarily an insurance program, not a foreclosure action. The real issues are eligibility during life and potential recovery after death, plus whether the home must be sold to pay for care.

If you are trying to start the family conversation without it turning into an argument, this resource can help: Discussing Your Parent’s Financial Future.

Once the myths are out of the way, you can follow a clear, repeatable process.

Step-by-Step Medicaid Asset Protection Guide for Brooklyn Homeowners

A good plan follows a client journey, not a pile of documents. Below is a step-by-step Medicaid asset protection guide that mirrors what many Brooklyn families experience from the first call to implementation.

Step 1: Get the facts on paper before you “do something”

You cannot protect what you have not inventoried. Gather deeds, co-op proprietary leases, mortgage statements, insurance, tax bills, bank statements, retirement accounts, and any business ownership documents.

A practical starting point is to confirm you are working with accurate numbers, not guesswork. This checklist-style article can help you organize: Is Your Financial Information Up to Date?.

Step 2: Identify the care path and the urgency

Medicaid strategy changes depending on whether care is at home, assisted living, or nursing home level. A family in Sheepshead Bay might be managing home care now but anticipating a nursing home later. Another family may be facing a hospital discharge and need a plan quickly.

New York may allow coverage to be applied retroactively in some situations, which can be a financial lifesaver when timing is tight. See: Using Retroactive Medicaid Benefits to Prevent Financial Disaster.

Step 3: Understand the lookback and transfer penalty risk

Many transfers are not “illegal,” but they can be penalized. For nursing home Medicaid, New York applies a lookback period that examines certain gifts and transfers. If a transfer is found, Medicaid can impose a penalty period where it will not pay, even if you are otherwise eligible.

For general federal context on Medicaid administration, see: Medicaid.gov.

Step 4: Choose the right legal tools for your home and your family

The tool must match the risk. For many families focused on how to protect home equity for Medicaid eligibility, a properly drafted irrevocable trust (often called a Medicaid Asset Protection Trust) is a common strategy, but not the only one.

If you are exploring trusts, this plain-English Q&A is a strong primer: When should a family consider a trust as part of an estate plan, and what type of trust should they use?.

Step 5: Execute, then “fund” the plan correctly

Signing papers is not the finish line, funding is. In real life, the work includes recording deeds, updating beneficiary designations, retitling accounts where appropriate, and creating a documentation trail that can survive Medicaid review.

If the home is being transferred into a trust, families often ask this exact question: Should I put my primary residence in an irrevocable trust?.

Step 6: Build the caregiver support plan around the legal plan

Legal planning works best when the caregiver is not burning out. A stressed caregiver is more likely to make rushed decisions, miss deadlines, or sign the wrong paperwork during a crisis.

For practical caregiver strategies, see: 10 Strategies to Thriving as a Caregiver.

This is where Brooklyn families often realize the next challenge: what if the home value is far above typical expectations?

Brooklyn Medicaid Asset Protection Strategies for High-Value Homes

High-value neighborhoods create high-stakes choices, even for families who feel “cash poor.” In areas like Brooklyn Heights, Park Slope, and DUMBO, the home value alone can drive the Medicaid conversation.

One case we commonly see is a small business owner who also owns the family home. The business cash flow is decent but irregular. The mortgage may be low because the home was bought decades ago. On paper, the home equity can look enormous, which can collide with Brooklyn high-value home Medicaid rules.

Strategies that are often used (and why they matter)

Brooklyn Medicaid asset protection strategies are most effective when they are layered. Depending on family goals and timing, a plan may include:

- Irrevocable trust planning: Used to shift future appreciation and protect the home from being consumed by long-term care costs, if done early enough.

- Spend-down with purpose: Paying legitimate expenses, home repairs, accessibility modifications, debt, and certain prepaid arrangements can reduce countable assets without “wasting” money.

- Title and beneficiary alignment: Cleaning up ownership issues, avoiding accidental probate problems, and coordinating powers of attorney so someone can act when health changes.

A key warning: do not treat a home equity loan as a magic fix. Borrowing against the home can change liquidity, monthly obligations, and how Medicaid evaluates your overall situation. The right approach depends on your timing and your care plan.

Next, let’s talk about what you can do this week to start moving forward without getting overwhelmed.

Taking Action: How to Start Protecting Your Home Equity for Medicaid Eligibility

The fastest progress comes from a short, focused first phase, not a full “life overhaul.” If your goal is Protecting Home Equity in Brooklyn’s High-Value Neighborhoods for Medicaid Eligibility, you want momentum and accuracy.

Start with these practical moves:

1) Pick one decision-maker for the process. Families get stuck when six relatives debate every detail. Choose one point person, usually the caregiver or the spouse.

2) Clarify the two outcomes you care about. Most Brooklyn families want (a) quality care and (b) keeping the home in the family. Say that out loud at the start, it reduces conflict.

3) Stop informal gifting and “quick deed” ideas. If you are already in motion with transfers, pause and get advice, because the lookback consequences can be severe.

4) Schedule a planning conversation with an elder law attorney. In our experience, the consultation is where the fog lifts, especially when you bring documents and real numbers.

If you are wondering what an attorney actually does beyond drafting, this overview is helpful: What Can an Elder Law Attorney do For You?.

When the plan is in place, many families feel relief for the first time in months. They can focus on care, not panic.

Want a clear plan tailored to your neighborhood, your home value, and your family dynamics? Schedule a free consultation with Alatsas Law Firm: Schedule a Free Consultation

Frequently Asked Questions About Protecting Home Equity for Medicaid in New York

What is the home equity limit for Medicaid in NY?

New York can apply a home equity limit for certain Medicaid long-term care eligibility situations, meaning very high equity may prevent approval even if the home is your primary residence. The exact limit can change, and the right number depends on the program category and your facts. Confirm current limits before applying, and do not assume your Brooklyn home is “automatically exempt” just because it is a residence.

How do I protect my assets from Medicaid in NY?

You protect assets by planning early, using the right legal tools, and avoiding penalized transfers. For many families, that means structured strategies like an irrevocable trust, careful spend-down, and coordinated estate planning documents so someone can act when health declines. The best plans also consider taxes, creditor exposure, and family risks like divorce, because Medicaid planning should protect the family, not just win an application.

Does a home equity loan affect Medicaid?

Yes, a home equity loan can affect Medicaid because it changes your finances and documentation requirements. While borrowing may reduce “equity” on paper, it can increase cash on hand, create monthly payments, and trigger questions about where the loan proceeds went. If the proceeds sit in an account, they may be treated as countable resources. Before borrowing, get advice on how the loan fits into your overall Medicaid and asset protection strategy.

Your Next Steps for Protecting Home Equity in Brooklyn

Protecting Home Equity in Brooklyn’s High-Value Neighborhoods for Medicaid Eligibility is possible, but it has to be done on purpose and on a timeline. The families who get the best results are not the wealthiest, they are the ones who stop guessing and start documenting.

If you take only one step after reading this, gather your key documents and have a focused planning conversation. A well-built Medicaid plan protects your home and your peace of mind, so you can concentrate on care and family, not fear.

When you are ready, Alatsas Law Firm can help you turn the next right step into a complete, executed plan.